Electric Bike Finance UK: Moped & Motorcycle Guide

Flex Electric

The UK's #1 Electric Moped and Electric Motorbike dealer.

You’ve probably done the same maths most first-time riders do. The bike looks right. The running costs look sensible. It would make commuting easier, and for delivery work it could be the difference between keeping more of what you earn and watching fuel and maintenance eat into it. Then you see the upfront price and pause.

That’s where finance stops being a luxury and starts being a practical tool. For many UK riders, paying monthly is the only realistic way to get onto an electric moped or motorcycle without draining savings in one hit.

This guide sticks to electric motorcycles, electric mopeds, off-road electric motorcycles and kids’ electric motocross bikes. It does not cover pedal e-bikes. That matters, because a lot of “electric bike finance UK” advice online drifts into bicycle rules, bicycle schemes, and bicycle tax treatment that do not apply to road-legal electric mopeds and motorcycles.

Your Guide to Electric Motorcycle and Moped Finance in 2026

The finance side matters more than many riders expect because policy still makes these machines costlier to buy than they arguably should be. The UK electric bike market generated USD 2,574.5 million in 2025, and electric mopeds and motorcycles still face the full 20% VAT rate, which adds hundreds to the purchase price, while electric cars benefit from incentives, according to UK e-bikes market outlook data.

That gap creates a strange situation. Electric two-wheelers make sense for city travel, delivery work and local business use, but the upfront price can still put people off. Finance is often the bridge between “I’d like one” and “I can get one”.

Who this matters for

Different riders come to finance with different worries:

- Urban commuters usually want a fixed monthly payment and simple budgeting.

- Food delivery riders often care most about protecting cash flow.

- Small businesses want vehicles without tying up working capital.

- First-time riders need plain-English answers, not finance jargon.

A good finance agreement doesn’t just make a bike affordable. It makes the whole ownership decision easier to live with month after month.

What tends to confuse buyers

The biggest source of confusion is that people use “bike” to mean completely different things. A pedal-assist bicycle, a road-legal electric moped, and an electric motorcycle don’t sit under the same rules, and they don’t always fit the same finance routes either.

That’s why this guide focuses on the practical questions riders ask when they’re buying a moped or motorcycle in the UK:

- Which finance type suits me?

- What does 0% APR really save?

- What do lenders look for when I apply?

- What will I really pay beyond the monthly figure?

- Can I still get finance if my credit isn’t perfect or if I work in delivery?

Understanding Your Core Finance Options

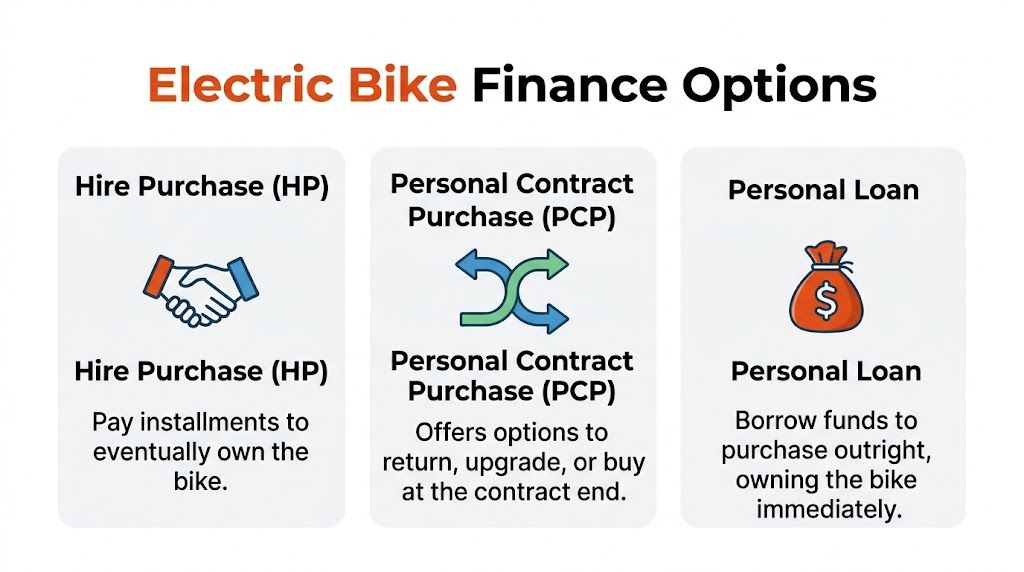

A lot of first-time buyers hear finance language and assume it is more complicated than it really is. In practice, you are usually choosing between three main routes for an electric moped or electric motorcycle in the UK: Hire Purchase, Personal Contract Purchase, and a personal loan.

The easiest way to sort them is to start with one real-world question. Are you buying a machine to keep for years, using it as a flexible stepping stone, or paying for it with borrowed money but owning it from day one?

One quick point before we get into the options. The Cycle to Work scheme is for bicycles and eligible e-bikes, not road-legal electric mopeds and motorcycles. That catches out plenty of buyers, especially commuters who search for "electric bike finance uk" and assume every two-wheeler fits the same rules. It does not.

Hire Purchase

Hire Purchase, or HP, is the clearest route to ownership. You pay a deposit, then fixed monthly instalments. At the end of the agreement, and after any option-to-purchase fee if one applies, the moped or motorcycle becomes yours.

For an urban commuter, HP often feels easiest because the destination is clear. You are paying toward ownership each month, like buying a work tool you plan to rely on for the long haul. That also makes HP popular with delivery riders and small businesses that want a vehicle they can keep using after the finance term ends.

Where HP makes sense

HP tends to suit riders who:

- Want ownership at the end and expect to keep the vehicle

- Prefer fixed payments and simple budgeting

- Use the bike for work and see it as a long-term asset

The upside and the trade-off

Pros

- Simple structure: Deposit plus monthly payments.

- Clear ownership path: The end goal is easy to understand.

- Useful for practical riders: Good for commuters, delivery riders, and businesses planning longer-term use.

Cons

- Monthly payments can be higher than some PCP deals.

- The commitment is firmer because you are working toward ownership.

- Leaving early may be less flexible than some buyers expect.

Personal Contract Purchase

PCP gives you lower monthly payments in many cases, because you are not paying off the full value in the same way as HP during the agreement. At the end, you usually choose between making a larger final payment to keep the bike, handing it back, or using any equity toward another vehicle.

This route can suit riders who want flexibility more than ownership. A commuter who is unsure whether a moped will still suit their routine in three years may like that choice. A rider considering a higher-spec electric motorcycle may also look at PCP to keep the monthly figure lower.

Practical rule: choose PCP because you want options at the end, not just because the monthly payment looks cheaper.

PCP usually suits riders who value flexibility

That might include:

- Riders who like changing vehicles every few years

- Buyers looking at higher-spec models

- People who are not sure they want to keep the bike long term

PCP pros and cons

PCP is more flexible, but it asks more of you at the end of the agreement.

- Monthly payments are often lower, which can help with affordability.

- End-of-term choices can be useful if your plans may change.

- The final payment matters if you decide you want to own the bike.

- Contract terms need closer attention, especially if you want clarity from the start.

For some riders, that flexibility is a real advantage. For others, it just adds another decision later.

Personal loan

A personal loan sits outside dealer finance. You borrow money from a bank or other lender, buy the electric motorcycle or moped outright, and then repay the loan separately. From the day you buy it, the vehicle is yours.

Some buyers like this because it keeps the purchase and the finance separate. If you already have a strong loan offer from your bank, it can feel straightforward. Small business owners sometimes look at this route too, especially if they want control over the purchase without using a dealer-linked agreement.

Why some riders prefer a loan

A personal loan can work well if:

- You want immediate ownership

- You have already found a competitive loan rate

- You prefer to arrange borrowing separately from the vehicle purchase

The catch is simple. Loan rates vary a lot. A good rate can make this route attractive. A poor rate can make it the most expensive option of the three.

A simple way to choose

A good finance agreement should match how the vehicle fits into your life.

If you are a commuter who wants predictable costs and plans to keep the bike, HP often makes the most sense. If you are a rider who may upgrade later, PCP can offer useful flexibility. If you are a buyer with access to a strong bank loan and want ownership straight away, a personal loan may suit you better.

Food delivery riders and small businesses usually benefit from looking past the smallest monthly figure. Cash flow matters, but so does what you are left with at the end. That is often the difference between a finance deal that looks good on paper and one that actually works in daily use.

Why Hire Purchase stands out at Flex Electric

A good 0% deal is clear and boring in the best possible way. You know the deposit. You know the monthly payment. You know when the agreement ends.

That clarity suits several types of rider:

- Urban commuters who want a predictable monthly cost instead of lumping all the expense into one upfront payment

- Food delivery riders who need to protect weekly cash flow and keep finance costs tight

- Learner riders buying a first road-legal electric moped or motorcycle and trying to keep the numbers easy to follow

- Small businesses adding one or more electric two-wheelers for local deliveries, site visits, or staff transport

For these buyers, the headline monthly payment is only part of the story. The stronger question is whether the total payable still looks sensible once the agreement finishes.

A lower monthly figure is helpful. A lower total cost is what really decides whether the deal works.

How dealer-arranged finance usually works

Dealer finance for electric motorcycles and mopeds is usually built around a few standard parts:

- A deposit, often required upfront

- A fixed term, so you know how long you will be paying

- A regulated lender, with checks on affordability and eligibility

- A credit assessment, because 0% finance still needs approval

Specialist dealers help because the finance is set up around road-going two-wheelers, not generic borrowing. That matters if you are comparing a commuter moped, a delivery workhorse, or a small fleet purchase. The right structure depends on how the vehicle will earn its keep or save you money.

A short explainer helps here:

Where buyers get caught out

The trap is assuming every tidy monthly payment is a good deal. It is not.

Some agreements look affordable because the term is longer than expected. Others require a larger deposit than the headline suggests. Some buyers focus so hard on the monthly figure that they miss the total payable, which is the number that tells you what the finance really costs.

Check these four points before you sign:

- Deposit required

- APR

- Monthly payment

- Total payable

A deal only makes sense if it is affordable now and still sensible when you add everything up.

Your credit profile also affects what you may be offered and whether an application is accepted. If you are unsure what lenders look at, this guide to the factors that affect a person’s credit rating gives a useful plain-English overview.

When 0% APR is a strong fit

0% APR tends to suit riders who expect to use the vehicle regularly and get practical value from it straight away. Daily commuters often fit that pattern. Delivery riders often do too, because the vehicle is tied directly to income. Small businesses can benefit for the same reason, especially if an electric moped or motorcycle helps reduce fuel, maintenance, or parking costs on local trips.

It is less useful if the payment would still stretch your budget too far. Interest-free finance is cheaper than interest-bearing finance, but it is still a commitment.

Used properly, 0% APR is one of the simplest ways to buy an electric motorcycle or moped in the UK without turning a sensible purchase into an expensive one.

Navigating the Finance Application Process

Finance applications feel more intimidating than they really are. Most of the stress comes from not knowing what the lender wants to see.

In the UK electric bike finance market for two-wheelers, lenders commonly look for applicants who are 18+, have at least 3 years of UK residency, can pay by direct debit, and can provide proof of identity and address, as described in this V12-linked e-bike finance overview. Those checks are there to confirm who you are, where you live, and whether the agreement looks manageable.

What you’ll usually need

Get these ready before you apply and the process becomes much smoother:

- Proof of identity such as a passport or driving licence

- Proof of address such as a recent bill or statement

- Bank details for direct debit

- Employment and income details if requested

- Your address history if you’ve moved recently

A lot of online applications are straightforward, but simple doesn’t mean careless. Small mistakes can slow things down.

How to give yourself the best chance

You don’t need to be a finance expert. You do need to be organised.

- Check your details carefully: Names, addresses and dates need to match your documents.

- Use your current address consistently: If your bank, licence and application all show different versions, lenders may pause the application.

- Be realistic about affordability: Apply for a monthly payment you can comfortably maintain.

- Review your credit profile beforehand: If you’re unsure what may influence a lender’s view, this guide to factors that affect a person’s credit rating gives a helpful plain-English overview.

If a lender asks for more information, that isn’t automatically bad news. It often just means they need to verify something before making a final decision.

What the process often looks like

Most buyers go through a sequence like this:

- Choose the vehicle and deposit

- Submit the online application

- Wait for the lender’s initial decision

- Provide any requested documents

- Review the agreement carefully before signing

Common reasons applications go wrong

The most common problems are boring ones, not dramatic ones. Incorrect addresses, incomplete employment details, mismatched bank information, or applying for a payment level that doesn’t fit your circumstances can all cause issues.

If you work in delivery or have a less conventional income pattern, honesty matters even more. Lenders don’t expect every applicant to fit a textbook salary profile, but they do expect accurate information.

A clean application won’t guarantee approval, but it does remove avoidable problems. That alone can make the whole process feel much less stressful.

Calculating the True Cost of Your Electric Motorcycle

You spot an electric moped advertised at a monthly figure that looks manageable. Then real life joins the conversation. Insurance, charging, security kit, and a deposit can change what "affordable" means.

That is why the true cost needs a wider lens than the finance payment alone.

A clear way to price an electric motorcycle or moped is to treat it like three separate pots of money. First, the upfront cost, usually your deposit and any day-one extras. Second, the monthly commitment, which is your finance payment plus running costs. Third, the setup choices that affect convenience, especially charging and security.

How deposits and terms change the picture

A deposit does two jobs. It reduces how much you borrow, and it can make the monthly payment easier to live with. The trade-off is simple. More paid upfront usually means less pressure each month.

Term length changes the shape of the cost rather than the total on a 0% APR deal. A shorter term is like taking bigger steps to reach the finish sooner. A longer term uses smaller steps, but you keep making them for longer. Neither is automatically better. It depends on your cash flow.

Here is a simple example using a £2,999 electric moped with a £500 deposit on a 0% APR basis:

Vehicle PriceDepositAmount to FinanceTerm (Months)Monthly Payment£2999£500£249912£208.25£2999£500£249924£104.13

The maths is straightforward because there is no interest added in this example. Divide the amount financed by the number of months, and you get the monthly payment.

Costs outside the finance agreement

This is the part first-time buyers often underestimate, especially riders comparing electric mopeds with petrol scooters or reading generic electric bike finance UK advice that is really about bicycles.

- Insurance: Cost depends on your age, postcode, licence, storage, claims history, and vehicle class. Get quotes before you commit to a model.

- Charging: Electricity is usually cheaper than petrol, but your actual routine matters more than the headline. Home charging is different from relying on public points.

- Security and riding kit: A proper lock, helmet, gloves, weatherproof gear, and sometimes a top box are day-one purchases for many riders.

- Servicing and wear items: Electric motorcycles and mopeds avoid some petrol-bike maintenance, but tyres, brake pads, suspension, and general checks still cost money.

Charging costs need practical thinking.

The useful question is not just "What does one charge cost?" Ask "Where will I charge, how often, and how convenient will that be after a month of real use?" An urban commuter with off-street parking has a different answer from a delivery rider in a flat, and a small business running several mopeds has a different answer again.

If home charging is part of your plan, setup cost matters as well as electricity cost. For background reading, this guide to home EV charger installation costs helps explain the practical side of getting charging in place.

A low monthly payment can still strain your budget if insurance, charging, locks, and riding gear were never part of the plan.

A simple budgeting method

Use one page and write down these three figures:

- Your monthly finance payment

- Your expected monthly running costs

- Your one-off setup spending

That gives you a far more honest ownership number than the advert alone.

For example, a commuter may care most about keeping the full monthly total predictable. A food delivery rider may focus on whether the bike earns more than it costs each week. A small business may care about total fleet cost, downtime, and whether putting down a larger deposit protects cash flow later.

The cost questions worth asking before you buy

Use this checklist before signing anything:

- Would a larger deposit make the monthly budget more comfortable?

- Does the shorter term genuinely suit my income, or do I just like clearing finance faster?

- Have I checked insurance on this exact type of electric motorcycle or moped?

- Will I charge at home, at work, or on public infrastructure?

- Do I need luggage, delivery equipment, or stronger security from day one?

- Am I looking at a motorbike or moped finance deal, rather than bicycle finance or Cycle to Work advice that does not apply here?

That last point catches a lot of first-time buyers out. The Cycle to Work scheme is designed for bicycles and e-bikes, not road-legal electric motorcycles and mopeds. If you are financing an electric moped for commuting, delivery work, or business use, you need to judge it like a motor vehicle purchase, with motor insurance, vehicle running costs, and a finance structure that fits how you ride.

Finance Solutions for Every Rider

A rider in central London may need a cheap, reliable way to get to work every day. A delivery rider may need a bike that earns its keep six nights a week. A small business owner may need two or three electric mopeds without draining cash from the business account. Those are three very different jobs, so they need three different finance conversations.

Generic "electric bike finance UK" advice often blurs everything together. That is where first-time buyers get caught out. A road-legal electric moped or motorcycle is financed like a motor vehicle, not like a pedal bike, and the right option depends heavily on how you will use it.

If your credit history isn’t perfect

Plenty of riders assume bad credit means an automatic no. It does not. What it often means is that your choice of lender narrows, the checks may be stricter, and the APR can rise sharply.

That last part matters most.

A higher APR can make an affordable-looking electric moped much more expensive over the full term. The monthly payment may still look manageable at first glance, but the total repayable can climb quickly. For a first-time buyer, that is a bit like spotting a low weekly phone contract without noticing how long the contract runs and what you pay overall.

The practical approach is simple:

- Check the representative APR carefully

- Look at the total amount payable, not only the monthly figure

- Be honest about what you can still afford in a slower month

- Avoid rushing into the first approval if the terms are poor

A yes is only useful if the agreement stays comfortable after the excitement of buying the bike has worn off.

What delivery riders should focus on

For food delivery riders, an electric moped is not just transport. It is income equipment. That changes the finance test.

A salaried commuter might ask, "Can I fit this into my monthly budget?" A delivery rider should also ask, "Will this payment still feel safe if orders dip for two weeks?" That is the right way to judge it, because gig work income can move around from week to week.

Preparation helps a lot here. Lenders usually want a clear picture of your earnings and employment status, so messy records can slow things down or weaken your application.

A delivery rider is usually better off doing four things before applying:

- Keep bank statements and income records tidy

- State your work type accurately

- Choose a payment level that leaves breathing room

- Treat high-interest offers with extra caution

If the agreement only works in a very busy month, it is too tight.

Cycle to Work does not cover electric mopeds and motorcycles

This is one of the biggest points of confusion for UK buyers.

Cycle to Work is aimed at bicycles and compliant e-bikes. It does not apply to road-legal electric mopeds and electric motorcycles. So if you are reading bicycle finance guides and trying to apply that advice to a delivery moped or commuter scooter, you are starting from the wrong rulebook.

That misunderstanding affects three groups again and again:

- Urban commuters who assume any electric two-wheeler counts

- Delivery riders who hope salary sacrifice can reduce the cost of a moped

- Small businesses looking at electric delivery vehicles for staff use

There is another practical limit. Salary sacrifice schemes also do not suit everyone who needs low-cost transport, particularly people who are not paid through a standard employer payroll. For self-employed riders, many gig workers, and people outside regular PAYE employment, motor vehicle finance is usually the more relevant route to examine.

Business and fleet use

For a takeaway, florist, estate agent, venue, or local service company, financing electric mopeds can make more sense than paying for every vehicle upfront. It spreads the cost in the same way businesses spread the cost of other working assets, which helps protect cash for stock, wages, rent, and day-to-day surprises.

That matters more than many owners expect. A business can like the idea of going electric, then stall when it sees the upfront bill for multiple machines, boxes, locks, and setup kit. Finance can turn that from one large hit into a planned operating cost.

For business buyers, the key questions are usually practical:

- How many vehicles do we need now, not in theory?

- Would keeping more cash in the business help more than buying outright?

- Are the monthly payments easier to absorb than a single large purchase?

- Will these mopeds be used often enough to justify the agreement?

A financed vehicle that is out on the road earning money or supporting staff travel is easier to justify than one that ties up capital before it starts delivering value.

Matching the finance route to the rider

The best finance choice starts with the actual job the bike needs to do.

Rider typeMain priorityFinance mindsetUrban commuterPredictable monthly outgoingsLook for clear payments and a manageable total costFood delivery riderProtecting weekly earningsLeave margin for quieter periods and be careful with high APRSmall businessPreserving working capitalCompare monthly cash flow against buying outrightFirst-time riderClarity and confidenceChoose simple terms you can explain back in plain EnglishEnthusiastChoice and flexibilityMatch the agreement to whether you want to keep or change bikes later

Good finance advice for electric motorcycles and mopeds should sound specific, not generic. If the deal fits your riding pattern, your income, and your actual reason for buying, you are much more likely to end up with a bike that helps rather than a payment that nags.

Start Your Electric Journey Today

Financing an electric moped or motorcycle doesn’t need to be confusing. Once you strip away the jargon, you’re really choosing between a few practical questions. Do you want to own the bike at the end, keep your options open, or buy outright from day one? Do you want the lowest monthly figure, or the lowest total cost?

For many riders, the standout option is still Hire Purchase when it’s available and affordable. It keeps the numbers cleaner, avoids interest, and makes a higher upfront vehicle price easier to handle month by month.

The important thing is to judge the whole picture. Look at the deposit, the monthly payment, the total payable, and the costs around ownership such as insurance, charging and kit. If you’re a commuter, a delivery rider, or a business owner adding electric two-wheelers to your operation, that honest view gives you a much better buying decision than the headline finance advert alone.

A good finance agreement should make your life easier, not more complicated. If the numbers are clear and the monthly payment is comfortable, going electric becomes much more achievable than many first-time buyers think.

If you're ready to compare models, ask finance questions in plain English, or see what a realistic monthly payment could look like, take a look at Flex Electric. They specialise in electric mopeds, scooters, motorbikes, off-road models and kids’ MX bikes, and they offer straightforward help without the usual finance waffle.

Find us

You will find us at 74 Dalry Road, Edinburgh, EH11 2AY

Showroom Opening Times:

Monday: By Appointment

Tuesday to Friday: 11am - 5:00pm

Saturday: 10am - 5pm

Sunday: By Appointment