Electric Motorcycle Insurance in the UK: Everything You Need to Know

Flex Electric

The UK's #1 Electric Moped and Electric Motorbike dealer.

You've probably just done the fun part. You've narrowed your shortlist, compared specs, and started imagining your daily run on something cleaner, quieter, and cheaper to run than a petrol bike. Maybe you're eyeing a sleek commuter, maybe a delivery-ready workhorse, maybe a serious machine you want to keep for years.

Then the boring bit shows up. Insurance.

Treat that as a mistake and you'll either overpay, buy the wrong cover, or miss the one exclusion that catches electric owners out later. Get it right and your bike becomes usable, legal, and properly protected from day one. That matters whether you're buying your first electric moped or moving into a full electric motorbike with real performance.

Your Key to the Road

A new electric motorbike feels like a smart move the moment you sit on one. Quiet pull-away, low running costs, no fuel station routine, and a setup that makes a lot of sense for city riding. That's why more commuters, delivery riders, and small businesses are looking seriously at electric two-wheelers instead of treating them like a novelty.

But there's one step that decides whether you're ready to ride or just own a machine that stays parked. You need the right electric motorbike insurance.

This isn't admin for admin's sake. It's what enables legal road use and protects you from the kind of costs that can turn a good purchase into a painful one. If you buy the cheapest policy without understanding what it does and doesn't cover, you can still end up exposed.

Practical rule: Buy insurance based on how you'll actually use the bike, not just the lowest quote on the screen.

For a new owner, that means getting clear on four things:

- Your legal position: whether your bike needs registration, tax, a licence, and insurance

- Your cover level: third-party only, third-party fire and theft, or full coverage

- Your electric-specific risks: battery cover, charging accessories, theft, and declared modifications

- Your long-term costs: especially exclusions most riders don't spot until it's too late

If you understand those properly, you'll make better decisions than most buyers do.

UK Legal Requirements for Electric Motorbikes

You buy the bike, charge it overnight, and plan your first ride to work. Then you find out the law does not care that it is electric. If it falls outside the EAPC rules, it is treated as a moped or motorcycle, and the road rules are the same ones that apply to petrol bikes.

That point catches new owners all the time. If your two-wheeler has no usable pedals, goes beyond the EAPC power or assisted speed limits, or is built as a road-going electric motorbike from the outset, you should assume it needs the full motorcycle setup. That means registration, tax, the right licence, a helmet, and at least third-party insurance before you use it on public roads.

What the minimum legal cover actually means

The legal minimum is third-party insurance. It pays for injury or damage you cause to other people. It does not pay to repair or replace your own bike after a crash, theft, or battery-related problem.

That distinction matters more with electric motorbikes because replacement costs can be painful. A rider who only focuses on getting legal can miss the bigger financial risk, especially around the battery. Standard policies often protect you against sudden insured events, but they do not pay for gradual battery degradation. Insurers rarely put that front and centre. You need to spot it yourself before it becomes an expensive surprise.

If you ride uninsured, the penalties are harsh. You can face a fixed £300 fine, at least six penalty points, disqualification, and seizure of the bike. If the case goes to court, the penalties can go further, as set out by Carole Nash's guidance on electric motorbike insurance.

My advice to new electric riders

Sort the legal basics before you spend time comparing extras.

Use this checklist:

- Confirm whether the bike is legally an EAPC or a motor vehicle

- Arrange insurance before the first road ride

- Make sure your licence matches the bike category

- Check whether the policy wording says anything useful about the battery, charging cable, and theft protection

- Do not assume "electric" means special treatment from the law

The blunt version is simple. If the bike is a motorbike in law, insure it like a motorbike. Then read the exclusions properly, because being road-legal is only the starting point.

Choosing Your Level of Cover

Most riders make this decision badly. They either buy the cheapest policy and regret it later, or they buy the fullest cover available without asking whether it suits the bike. You need to match the policy to the machine and to the way you ride.

Think of the three main insurance tiers like levels of security. One covers the legal basics. One protects against the most common ownership headaches. One is the strongest overall shield.

Electric Motorbike Insurance Tiers Compared

CoverageThird-Party OnlyThird-Party, Fire & TheftFully ComprehensiveDamage or injury to othersYesYesYesFire damage to your bikeNoYesUsually yesTheft of your bikeNoYesUsually yesDamage to your own bike after an accidentNoNoUsually yesBest fitLegal minimum on a lower-value bikeRiders who want theft and fire protection without full coverNewer, higher-value, or harder-to-replace bikes

Third-party only

This is the legal floor. It's there to make you road-legal, not to protect your investment.

If you're riding an older or lower-value machine and you'd be comfortable accepting the financial hit if it were stolen or damaged, third-party only can be a rational choice. That's especially true for some occasional riders. But don't kid yourself that it's broad cover. It isn't.

Third-party, fire and theft

This is the middle ground and often the sensible one. It gives you the legal third-party cover you need, plus protection if the bike is stolen or damaged by fire.

For urban riders, this tier often deserves more attention than it gets. Theft is one of the biggest practical worries with any two-wheeler, and electric models aren't exempt. If you'd struggle to replace the bike yourself, this level makes more sense than bare-minimum cover.

Fully comprehensive

If the bike is expensive, new, financed, or difficult to replace, this is usually the right answer. Fully protective policies can also include options such as battery cover, charging cable cover, breakdown assistance, and riding gear cover, as outlined in MoneySuperMarket's electric motorbike insurance guide.

That doesn't mean every policy includes the same extras. You still need to read the wording. But this is the tier I'd push most buyers towards if they're stepping into a serious machine.

A good example is the Vmoto Stash. Its published snapshot describes a machine designed by Adrian Morton with a 75 mph top speed, a 15kw motor, and up to 110mile range. That sort of bike deserves proper cover. Buying a premium electric motorbike and protecting it with the legal minimum is usually false economy.

If losing the bike would create a serious financial problem, don't insure it like a disposable runabout.

How Electric Bike Insurance Is Different

You buy an electric motorbike, park it outside a café, and do the sensible thing by arranging insurance the same day. Months later, the battery starts losing range far faster than you expected. That is usually where riders discover the gap. Insurance may pay for theft or sudden damage, but it almost never pays for battery degradation, and many insurers do not spell that out clearly.

Battery cover needs real scrutiny

Start with the battery, because it is the most expensive part riders misunderstand.

A policy might cover battery theft. It might cover damage caused by a crash, fire, or another insured event. That is useful, but it is not the same as cover for gradual decline in battery health. If capacity drops over time, you are usually looking at wear, not an insurable loss. That cost often lands on you unless a separate manufacturer warranty applies.

Ask for the answer in plain English. Does the policy cover theft, accidental damage, water damage, and fire damage to the battery? Does it exclude deterioration in performance, reduced charging capacity, or normal aging? If the insurer cannot answer clearly, move on.

Charging kit and electric-specific parts

Electric motorbikes come with parts petrol bikes do not. Charging cables, portable chargers, wall units, and battery connectors can all be expensive to replace. Some policies include them. Others treat them as accessories with low limits, or do not cover them away from home.

Do not assume they are automatically protected.

Ask these questions before you buy:

- Are charging cables covered at home and away from home?

- Is the charger treated as part of the bike or as a separate accessory?

- Are battery connectors and control units covered if damaged in a theft attempt?

- What single-item limit applies to electric accessories?

Theft risk needs a harder look

Electric bikes suit urban riding, and that often means more time parked in public. Insurers care about storage, locks, alarms, trackers, and whether the bike stays on the street overnight. They also care about how easy the bike is to move if thieves get access to it.

That is why security conditions matter so much. If a policy requires an approved chain, ground anchor, alarm, or tracker, meet that condition exactly. A good car anti-theft monitoring system can also help you think more seriously about how tracked security works in practice, especially if you keep the bike in a higher-risk area.

Modifications and declared extras

Electric owners often add useful kit early. Top boxes, luggage systems, upgraded locks, phone mounts, heated grips, and cosmetic parts can all affect a claim if they are not declared properly.

Do not guess what counts as a modification. Ask the insurer what must be listed and get it noted on the policy. That matters even more on electric models, where added security devices and charging equipment can blur the line between standard equipment and extras.

The expensive mistake is assuming “battery cover” means the insurer will pay when the battery simply gets worse over time. It usually means the exact opposite.

What Drives Your Premium and How to Reduce It

You buy the bike, sort the charger, then the quote lands and the number is higher than expected. That usually happens for a simple reason. Insurers are pricing theft risk, repair cost, rider profile, and replacement value. On an electric motorbike, they are also pricing uncertainty.

What insurers are really pricing

Start with the basics. Your age, licence type, riding history, postcode, annual mileage, where the bike sleeps, and the bike's value all feed into the quote.

Electric models add another layer. Parts can be expensive, approved repairers can be harder to find, and some insurers still treat newer or less common models cautiously. That caution shows up in the premium.

Battery value matters too, but in a way many riders misunderstand. A costly battery can push the replacement value up. It does not mean the policy will pay out because the battery loses capacity over time. Degradation is usually your problem, not the insurer's. That gap catches owners out, and it should shape how you judge a quote.

Cheap quotes can cost you more

A lower premium often means one of four things. A bigger excess. Tighter theft conditions. Weaker cover for accessories and damage. Or an insurer that does not properly understand the bike.

That last one matters. If the call handler cannot clearly explain how the policy treats the battery, charging cable, or fitted accessories, do not reward that confusion with your business.

The best ways to cut the price

Use the factors you can control.

- Improve security: Fit quality locks, alarms, or a tracker, and make sure the insurer records them correctly.

- Park off-street if you can: A locked garage usually beats driveway parking, and driveway parking usually beats leaving the bike on the road overnight.

- Choose the right excess: A voluntary excess can reduce the premium, but only set it at a figure you could pay without stress after a claim.

- Limit unnecessary mileage: If you ride 3,000 miles a year, do not insure it as if you ride 10,000.

- Avoid undeclared modifications: Added screens, luggage, security kit, and cosmetic parts can affect claims and pricing.

- Use specialist insurers: Electric motorbikes still confuse parts of the market. A specialist often prices them more fairly.

Security is where new owners can save real money. Good storage and visible anti-theft measures reduce risk before you even ask for a discount. For riders comparing trackers and alerts, it helps to understand how modern car anti-theft monitoring systems work, because the same principles apply when you are judging movement alerts, location tracking, and theft response for a bike.

My advice if you want lower premiums without hollow cover

Start by deciding what you cannot afford to lose. If replacing the bike would hurt, buy cover that protects the bike properly and then bring the premium down through storage, security, mileage, and a sensible excess.

Do not strip the policy back so far that one theft or one serious accident turns a saving into a loss. And do not let the word "battery" on a policy summary fool you. Check whether it covers sudden insured damage or theft, then ask separately about the long-term problem insurers rarely highlight. Battery degradation.

Here's a useful video if you want a broader feel for electric motorcycle ownership and the cost conversation before you lock in a policy:

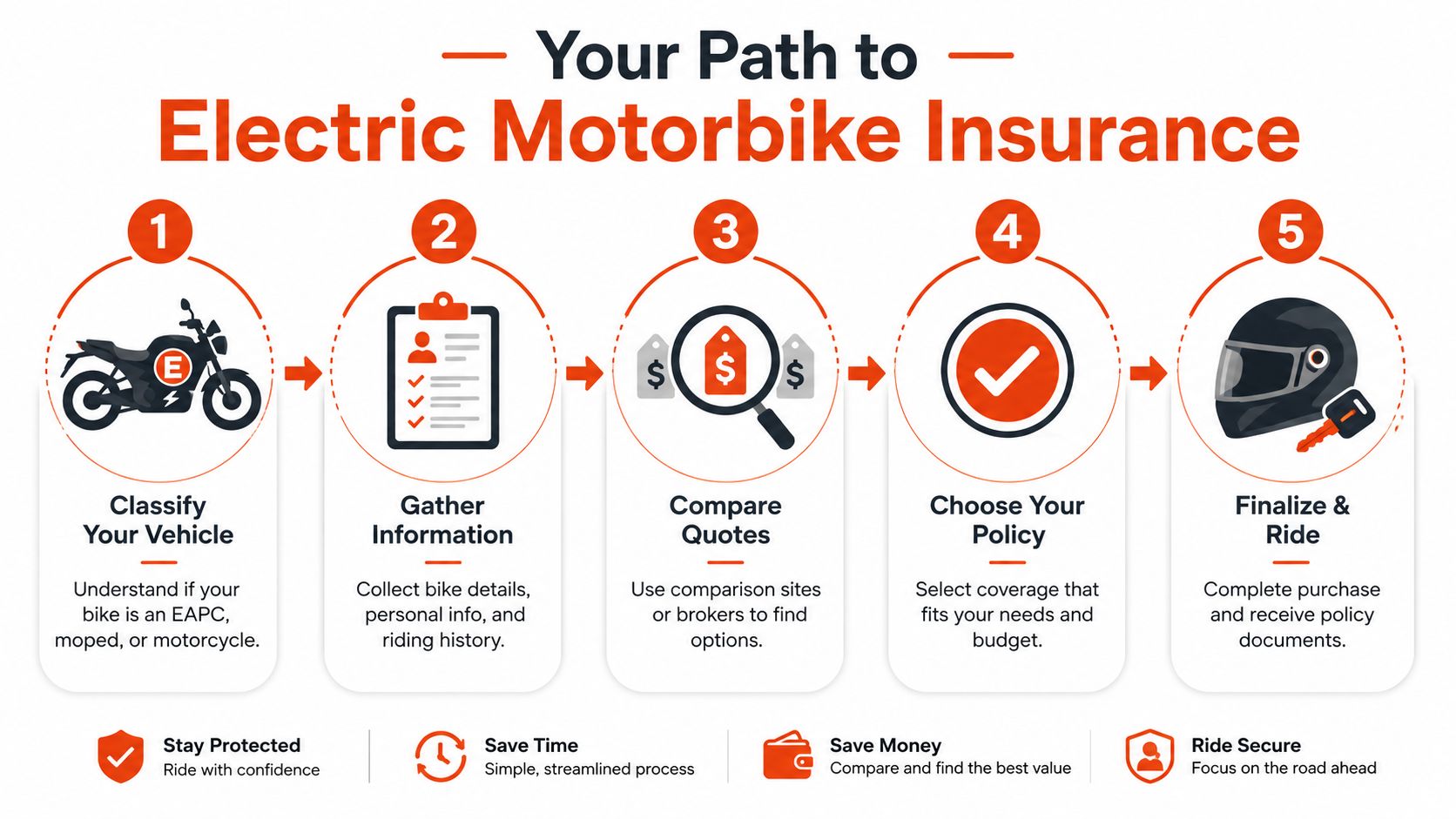

A Step-by-Step Guide to Getting Insured

You buy the bike, sort the charger, plan your first ride, then hit the quote form and get stuck. The insurer asks what the bike is, how it's stored, what it's used for, and whether the battery is covered. Get any of that wrong and you either overpay or buy a policy that lets you down when you need it.

Start with the classification. If your bike does not fall under EAPC rules, insure it as a motorcycle or moped, not as a bicycle. That sounds basic, but it is one of the easiest ways to spoil a quote or create trouble later if you need to claim. As noted earlier, the legal category determines what paperwork and insurance the bike needs.

Next, get your details in order before you ask for quotes. Have your licence details ready. Have the registration and V5C if the bike is already on the road. Know exactly where it will be kept overnight, and list every security device fitted to it. Sloppy applications cause avoidable problems.

Then compare quotes like a broker would. Ignore the headline price for a minute and check the parts that decide whether the policy is any good. Look at the cover level, the excess, the exclusions, the theft terms, and whether the insurer is comfortable with your exact model. Electric bikes still get misread by parts of the market.

Your usage matters just as much. A rider commuting into town, a rider using the bike for weekend trips, and a rider doing delivery work need different cover. If the declared use does not match reality, the policy can fail at the worst time.

Use this checklist before you buy:

- Confirm the legal category: Do not guess whether the bike counts as an EAPC.

- Prepare your documents: Licence, registration details, address history, and storage details.

- Declare modifications properly: Top box, pannier rack, alarm, tracker, heated grips, and other add-ons all matter.

- Ask electric-specific questions: Is the battery covered for theft or accident damage? Are the charging cable and portable charger covered? What about accessories?

- Ask the question insurers often skate past: Does the policy cover sudden battery damage only, or are you being left to carry the cost of battery degradation later?

- Use a specialist early for higher-value or higher-performance bikes: It saves time and usually produces better answers.

That fifth point matters more than many new owners realise. A policy can mention battery cover and still leave out battery degradation, which is one of the biggest long-term costs on an electric motorbike. Do not accept vague wording. Ask for a plain-English answer before you pay.

Buy the policy only when you can explain it back in simple terms. What is covered. What is excluded. What excess applies. What use is allowed. If any of that is unclear, stop and ask again.

There is also a practical market issue. Some mainstream insurers still hesitate on higher-performance electric bikes, which pushes riders toward specialist providers earlier than they expect. That is usually the right move, not a last resort.

Critical Exclusions and Special Considerations

This is the part most generic guides gloss over, and it's the part that matters most if you plan to own the bike for more than a short spell.

The battery degradation trap

A standard policy may mention battery cover and still leave you exposed to one of the biggest ownership costs. The critical exclusion is battery degradation.

According to Lexham's electric motorcycle and moped insurance page, battery degradation or failure due to wear and tear is not covered under standard electric motorbike insurance policies. The same source notes that this can leave owners facing battery replacement costs of £1,500–£2,000 for some models.

That matters because many riders read “battery cover” and assume long-term battery decline is included. It isn't. Insurance is designed for insured events, not normal ageing of a component.

Battery theft and battery wear are not the same problem. Don't buy a policy thinking it solves both.

Delivery use changes everything

If you're using the bike for food delivery, standard social, domestic, and pleasure cover isn't enough. You need the correct business use, and in many cases that means hire and reward cover. If you get this wrong, you can think you're insured when you're not insured for the work you are doing.

That's a serious issue for riders on platforms such as Deliveroo, Uber Eats, or Stuart. If the bike earns you money, tell the insurer exactly how.

Fleet and business ownership

For small businesses electrifying local transport, a one-bike private policy mindset isn't enough. Fleet operators should look at policy administration, driver use, storage arrangements, downtime risk, and whether accessories or delivery equipment need declaring.

If you're buying for work rather than personal use, don't force a consumer insurance template onto a business problem. Ask for commercial guidance from the start. That saves time and avoids ugly surprises when a claim lands.

FAQ for Flex Electric Riders

Does a battery warranty replace insurance

No. They do different jobs.

A warranty deals with specified defects or failures covered by the warranty terms. Insurance deals with risks such as accidents, theft, or other insured events under the policy. If you assume one replaces the other, you create a gap. That's especially important with electric bikes because battery-related language can mislead owners into thinking every battery problem sits under one umbrella. It doesn't.

Will I need specialist insurance for a higher-performance model

Often, yes. Not because the bike is unusual in legal terms, but because parts of the market still struggle to quote confidently on electric performance models. If you're looking at something faster, more expensive, or less common than an entry-level electric moped, go to specialist insurers earlier. It will save time.

What documents help the insurance process go smoothly

The basics are your licence details, bike registration details where applicable, storage information, and any security device details. If the bike is new to you, having the correct model information and supporting paperwork ready makes quote accuracy much better.

What if I'm buying for commuting and delivery

Tell the insurer both. Don't simplify your usage just to get the quote moving. The wrong declared use is one of the fastest ways to create claim trouble later.

Can the seller help with the insurance process

Yes, in practical ways. A specialist retailer can usually help you identify the correct bike category, provide model details, and supply supporting documents such as the Certificate of Conformity where relevant. That doesn't replace the insurer's underwriting decision, but it makes the application cleaner and faster.

If you're buying from Flex Electric, the useful part is straightforward support around model documentation, real-world bike specs, and the kind of ownership questions that matter before you apply for cover.

If you're choosing an electric motorbike and want straight answers on models, documents, and the practical details that affect insurance, Flex Electric is a sensible place to start. It stocks electric mopeds, scooters, motorbikes, and off-road models, and it can help you line up the right information before you go hunting for cover.

Find us

You will find us at 74 Dalry Road, Edinburgh, EH11 2AY

Showroom Opening Times:

Monday: By Appointment

Tuesday to Friday: 11am - 5:00pm

Saturday: 10am - 5pm

Sunday: By Appointment