Finance Motorcycles with Bad Credit: Your 2026 Guide

Flex Electric

The UK's #1 Electric Moped and Electric Motorbike dealer.

If you're reading this, there's a fair chance you've already talked yourself out of applying.

Maybe you need a reliable moped for delivery work. Maybe you're done with late trains and expensive buses. Maybe you've had missed payments in the past, your credit file isn't clean, and you assume finance is off the table. That worry is common, and in many cases it's based on an old idea of how lending works.

Today, when people try to finance motorcycles with bad credit in the UK, the conversation is usually less about a single score and more about whether the deal is affordable in real life. That's a much more useful standard for riders who are trying to get back on track.

A lender still cares about risk. No one should pretend otherwise. But a weak credit history doesn't automatically end the process. What matters is whether your income, regular commitments, and the bike you're choosing line up in a way that makes the monthly payments sustainable.

That matters even more in the electric moped and motorbike market. Buyers are often choosing these bikes for practical reasons. Commuting, delivery work, lower day-to-day costs, simpler transport in town. In those cases, the right finance application isn't about chasing the biggest bike you can technically apply for. It's about building a deal that stands a realistic chance of being approved and that you can keep comfortably.

Your Road to Riding Starts Here Not with Your Credit Score

A rider comes in wanting a bike for work. Their first sentence is often some version of, "I've got bad credit, so I probably won't get accepted."

That isn't always true.

In practice, a lot depends on what the lender sees today. If your income is steady, your outgoings are sensible, your address history is clear, and the monthly repayment fits your budget, you may have options even with a rough credit background. That's the part many people miss.

The problem with score-first thinking

People often treat their credit score like a final verdict. It isn't. It's a signal. It tells lenders there may be more risk, but it doesn't describe your whole situation.

A delivery rider earning consistently now may look very different from the version of themselves who missed payments during a hard patch. A commuter who had defaults a few years ago may now have stable housing and better budgeting habits. Lenders can see that difference if the application is structured properly.

Bad credit doesn't mean no chance. It usually means the margin for error is smaller, so the details of the application matter more.

What usually works better

The strongest bad-credit applications are rarely dramatic. They're tidy.

They usually involve a bike that fits the rider's actual needs, a monthly payment that isn't stretched, and paperwork that supports the story. If you're trying to finance motorcycles with bad credit, that's the mindset to adopt. Not "How do I get approved for anything?" but "What can I afford comfortably, and how do I prove it clearly?"

That approach helps in the electric market because smaller mopeds and practical urban bikes often line up better with affordability checks than a more expensive machine chosen on impulse.

What tends to go wrong

A few mistakes keep coming up:

- Applying before checking your file: You don't want to discover an old error only after a lender has reviewed you.

- Choosing the bike first: If you fall in love with a model before you know your budget, disappointment usually follows.

- Understating outgoings: Lenders look for consistency. If your figures don't make sense, trust drops quickly.

- Chasing "guaranteed" promises: Those offers often sound easier than they are.

There's a route forward for many riders with weak credit. It just starts with realism, not panic.

How UK Lenders Really View a Bad Credit Application

UK lenders don't assess motorcycle finance the way many applicants think they do. The old fear is that a computer checks a score, rejects the case, and that's the end of it. In reality, the process is more structured.

After post-2008 reform, affordability checks became a core lending requirement when the Financial Conduct Authority brought consumer credit under stronger conduct rules. Lenders now assess creditworthiness, income, and outgoings rather than relying on a single score, and the FCA Consumer Credit sourcebook requires a reasonable assessment of creditworthiness before lending, as outlined in this motorcycle finance overview of UK affordability checks.

What a lender is actually trying to answer

The key question isn't "Has this person ever had credit problems?"

It's closer to this: Can this person repay this agreement without running into difficulty?

That shifts the focus onto practical details:

- Income: Salary, self-employed income, or other regular income the lender can evidence

- Essential outgoings: Rent, mortgage, utilities, food, existing credit commitments

- Application stability: Address history, banking pattern, and consistency in the information you provide

- Loan structure: Deposit size, term length, and whether the monthly payment is sensible for your budget

For people with bad credit, this is good news and bad news at the same time. The good news is that older credit issues don't automatically kill the application. The bad news is that a lender will look hard at whether the proposed payment is realistically manageable.

Why soft-check tools can help

Before making a full application, it helps to understand what an eligibility tool is doing in the background. A plain-English guide to how bad credit eligibility checkers work is useful because it explains why some checks are designed to estimate suitability without committing you to a full lender decision straight away.

That matters if you're anxious about applying. You want as much clarity as possible before you step into a formal process.

Practical rule: The cleaner and more believable your affordability picture is, the more useful your application becomes to a lender.

Why the bike still matters indirectly

Lenders aren't mainly judging the bike as a fashion choice. They're judging the effect that bike has on the monthly payment and the risk of the deal.

A model like the Vmoto Stash sits at the performance end of the electric market. It was conceptualised by designer Adrian Morton, has a 75 mph top speed, a 15kw motor and up to 110mile range. For the right applicant that may fit, but for a weaker credit profile the main question is whether the numbers stay affordable once the finance is built.

That's why two riders with similar credit histories can get different outcomes. The stronger application is often the one that asks for a deal the lender can defend as affordable.

Your Realistic Motorcycle Finance Options with Poor Credit

Once you accept that affordability drives the decision, the next question is practical. What type of finance makes sense if your credit isn't strong?

For most UK riders, the conversation usually comes down to Hire Purchase, Personal Contract Purchase, or a deal involving a guarantor. Each has trade-offs. None is automatically right just because you have bad credit.

UK Motorcycle Finance Options Compared

| Finance Type | How It Works | Best For... | Key Consideration for Bad Credit |

|---|---|---|---|

| Hire Purchase (HP) | You pay a deposit if required, then fixed monthly payments across the term. Ownership usually transfers at the end once the agreement is completed. | Riders who want a straightforward path to ownership and a clear repayment structure. | Often easier to understand and manage, but a larger deposit or shorter term may help the case make more sense to a lender. |

| Personal Contract Purchase (PCP) | You pay monthly payments over the term with options at the end, which may include returning the bike or paying a final amount to keep it. | Riders who want lower monthly payments than a comparable ownership-focused deal may allow. | The end-of-term choice needs planning. If your budget is already tight, the structure can become awkward later. |

| Guarantor arrangement | Another person supports the agreement and may be liable if you don't keep up payments. | Applicants with weaker profiles who have a suitable guarantor willing to help. | This can improve access, but it shifts risk onto someone else, so both people need to understand the commitment fully. |

Hire Purchase often suits bad-credit buyers better

HP is often the most understandable route for people trying to finance motorcycles with bad credit. You know what you're paying each month, you know the term, and the deal is built around repaying the bike rather than managing a larger choice at the end.

That simplicity matters. If your file already gives a lender reasons to be cautious, a simpler structure can be easier to underwrite than a deal that depends on more moving parts.

HP can also work well for practical electric bikes bought for commuting or work. A rider looking at a Vmoto TS Street Hunter Pro may be considering a 125cc Equivalent Electric Motorbike with a top speed of 58mph and a 5kw peak power motor. In a case like that, the finance discussion is usually strongest when the monthly payment fits cleanly around the rider's regular commitments.

PCP can help monthly payments, but only if you plan ahead

PCP can lower the monthly figure compared with a more ownership-focused structure on the same bike. That's why some riders look at it first.

But lower monthly payments don't automatically mean the deal is safer. If your credit is poor, you don't want to focus only on getting the monthly amount down while ignoring the end-of-term decision. You need to understand what you'll do when the agreement finishes.

A PCP deal can make sense if you like flexibility and you're confident you'll manage the later choice sensibly. It makes less sense if you're applying from a financially stretched position and hoping to worry about the end later.

If the monthly payment only works because the future problem has been pushed down the road, the deal may not be as affordable as it first looks.

Guarantor support can help, but it changes the relationship

Some applicants look at a guarantor because they know their own file will make approval tougher.

That can be effective in the right circumstances, but it isn't a technical workaround. It's a serious commitment for the person backing you. If things go wrong, the strain isn't just financial. It can become personal very quickly.

For that reason, I usually see guarantor arrangements work best when both people understand the agreement in plain language and the rider could probably just about manage the bike anyway. The guarantor then strengthens the application rather than rescuing an unrealistic one.

One more useful lens from car finance

A lot of the basic risk logic is similar across vehicle lending. If you want a broader consumer-friendly explanation of how weaker-credit vehicle borrowing is handled, this guide on bad credit car loan help is useful for understanding the sort of issues lenders and applicants both weigh up.

What usually doesn't work

These approaches tend to end badly:

- Stretching for a bigger bike than you need: Higher monthly payments make the affordability case weaker.

- Choosing the longest term just to force a lower payment: That can help on paper, but not if the underlying budget is still too tight.

- Applying with unclear income: Especially for delivery riders or self-employed applicants, the lender needs a consistent picture.

- Picking the product before the budget: The finance type should fit your circumstances, not the other way round.

A workable deal is one you can live with after the excitement of collection day has passed.

A Checklist to Prepare Your Finance Application

A bad-credit application improves when the rider does the homework first. That's where you gain control.

A practical workflow is to obtain your statutory credit report from the UK credit reference agencies, correct any adverse data, then seek pre-approval before choosing the bike. Lenders and brokers commonly assess affordability using income verification plus credit-file checks, as described in this guide to preparing for motorcycle finance.

Start with your paperwork, not the bike

If your first move is browsing bikes, you're doing it in the wrong order.

Get your documents in one place first. That usually means proof of identity, proof of address, bank statements if requested, and evidence of income. If you're employed, that may be straightforward. If you're self-employed or doing delivery work, take extra care to present income clearly and consistently.

Your pre-application checklist

- Check your credit reports carefully: Look for incorrect defaults, addresses you don't recognise, duplicated accounts, or balances that should have been updated.

- Fix errors before applying: An application built on bad data is harder to save once it's underway.

- Write out your monthly budget accurately: Include rent, food, travel, utilities, current borrowing, and regular household costs.

- Think about deposit flexibility: Even a modest deposit can reduce the amount being financed and make the case easier for a lender to support.

- Seek pre-approval before choosing the exact bike: This helps you shop within a realistic budget instead of negotiating backwards from disappointment.

Why lenders care about presentation

A lender doesn't meet you in person. The application file has to do the work.

If the numbers line up, your address history is consistent, and your income picture is easy to follow, the lender can process the case with more confidence. If your documents are patchy and the spending pattern looks chaotic, even a potentially workable case becomes harder.

The aim isn't to make yourself look perfect. It's to make your situation understandable.

Match the bike to the evidence you can provide

This is especially important for riders buying for work. If you need a practical scooter for regular commuting or deliveries, choose something that supports that use case rather than making the application carry unnecessary cost.

For example, the Vmoto CPX 74V is described as a high-performance electric scooter built for commuting, delivery work and fleet use, with up to 87 mile range and 56mph top speed. For a rider whose income depends on daily urban use, a practical machine like that may be easier to justify in an affordability conversation than a more expensive or less relevant choice.

Before you submit anything

Ask yourself three blunt questions:

- Can I explain every major outgoing if the lender asks?

- Does this monthly payment still look comfortable after bills, not before them?

- Am I applying for the right bike, or just the bike I want most today?

That final question saves a lot of failed applications.

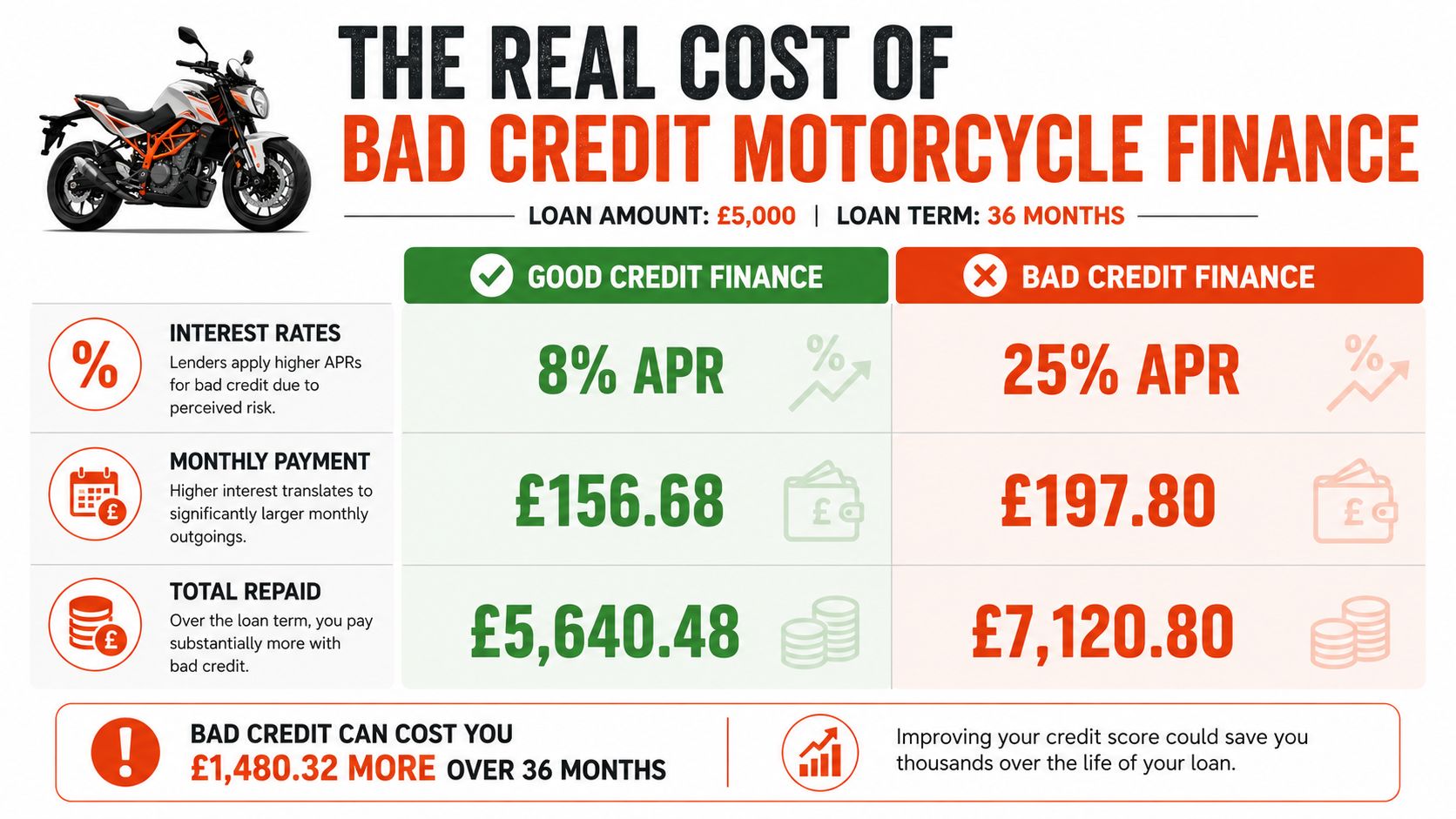

The True Cost of Bad Credit Motorcycle Finance

Bad-credit finance is possible for some riders, but it isn't cheap. That's how it is.

Motorcycle finance is harder and more expensive for borrowers with weaker credit because lenders price risk into the APR. A general score below roughly 670 sits below the stronger approval zone, while Experian notes scores run from 300 to 850 and 670+ is typically the "good" range, as summarised in this motorcycle loan and credit score guide.

The spread matters more than most buyers realise

If you're only looking at whether you can get approved, you're missing the harder question. What will this borrowing cost you?

One useful UK benchmark is the difference between average motor vehicle purchase APR and lower-score borrowing. UK consumer-credit figures referenced in this APR comparison for bad-credit vehicle borrowing show an average motor vehicle purchase APR of 11.3% in Q4 2024 versus 26.7% for lower-quartile score borrowers.

That gap is why a deal that looks manageable at first glance can become uncomfortable once the final monthly payment is set.

What that means in practice

When APR rises, a few things happen at once:

- Monthly payments get heavier: The same bike can move from reasonable to stressful.

- Total interest grows: You pay much more for the same machine.

- Your margin shrinks: Any change in income or living costs hurts faster.

- Refinancing isn't guaranteed: You can't assume you'll tidy it up later.

This is why I push riders to look beyond approval headlines. "Accepted" is not the same thing as "affordable".

A higher APR doesn't just change the total cost. It changes how much breathing room you have each month.

Don't ignore the insurance side

The finance payment isn't the only number that matters. You also need to budget for insurance, equipment, and day-to-day use. If you're comparing overall riding costs, The Ephraim Group's complete guide is a useful companion read because insurance can materially affect whether the bike remains manageable after finance is approved.

The safest bad-credit deal is usually the one that leaves room in the budget, not the one that pushes right up to the lender's limit.

Financing Electric Mopeds A Smart Route for Bad Credit

You need transport for work on Monday, your credit file is messy, and the bike you want still has to pass a lender's affordability checks. In that situation, an electric moped or small electric motorbike can be one of the more workable options in the UK market.

For bad-credit applicants, electric is often less about image and more about keeping the full monthly commitment realistic. A lower purchase price, lower fuel spend, and simpler day-to-day running costs can all help the application make sense on paper and in real life.

Why electric can improve the finance conversation

Lenders do not approve bikes in isolation. They look at whether the payment fits your current budget after rent, bills, existing credit, and regular living costs. That FCA-led affordability check matters just as much as the credit history itself.

A smaller electric machine can help in three practical ways. The amount borrowed may be lower. The projected monthly payment may sit more comfortably within your disposable income. The running costs are often easier to justify if the bike is mainly for commuting, city work, or replacing more expensive travel.

That does not mean every electric bike is easy to finance. Some models are still expensive, and PCP or HP only works if the numbers hold up under scrutiny. The advantage is that the electric market includes more low-commitment options than riders often expect, especially at moped and commuter level.

Where electric fits best

The strongest fit is usually a rider with a clear use case and a tight budget.

Electric mopeds and lightweight electric motorbikes often suit:

- Urban commuters who need dependable daily transport

- Delivery riders who want to keep ongoing costs under control

- First-time buyers who need an entry point that does not overstretch them

- Applicants with little or no deposit where a smaller machine gives the finance structure a better chance of passing affordability checks

I see this regularly. A rider comes in focused on getting any approval they can, but the better result is often choosing a cheaper, practical model that leaves room for insurance, charging, kit, and the unexpected.

What specialist lenders and dealers actually look at

Generic bad-credit advice tends to obsess over credit scores. Real underwriting is more grounded than that.

The useful questions are straightforward. What does your income look like month to month? Are your bank statements stable? Do you have recent missed payments, or older issues that are now settled? Is the bike for commuting to work, for business use, or for occasional leisure? Would a compact electric scooter do the job better than a larger motorbike that pushes the payment too far?

That is why a specialist electric dealer conversation can be more useful than a generic finance form. Flex Electric focuses on electric mopeds, scooters, motorbikes and off-road electric models, with Hire Purchase and PCP available and no minimum deposit required according to the company profile provided. For a bad-credit applicant, that matters because the stock itself is often better suited to affordability-led applications than a showroom full of higher-value petrol bikes.

A quick look at a real model helps make that concrete:

The smarter option is often the one you can keep comfortably

Bad-credit finance works best when the bike solves a transport problem without creating a budget problem.

A practical electric moped or commuter bike can be a sensible first step. You get mobile. You keep the monthly commitment more manageable. You give yourself a better chance of maintaining the agreement cleanly, which matters far more than forcing a bigger bike into the deal.

Find us

You will find us at 74 Dalry Road, Edinburgh, EH11 2AY

Showroom Opening Times:

Monday: By Appointment

Tuesday to Friday: 11am - 5:00pm

Saturday: 10am - 5pm

Sunday: By Appointment