Insurance for Electric Motorcycles: A UK Rider's 2026 Guide

Flex Electric

The UK's #1 Electric Moped and Electric Motorbike dealer.

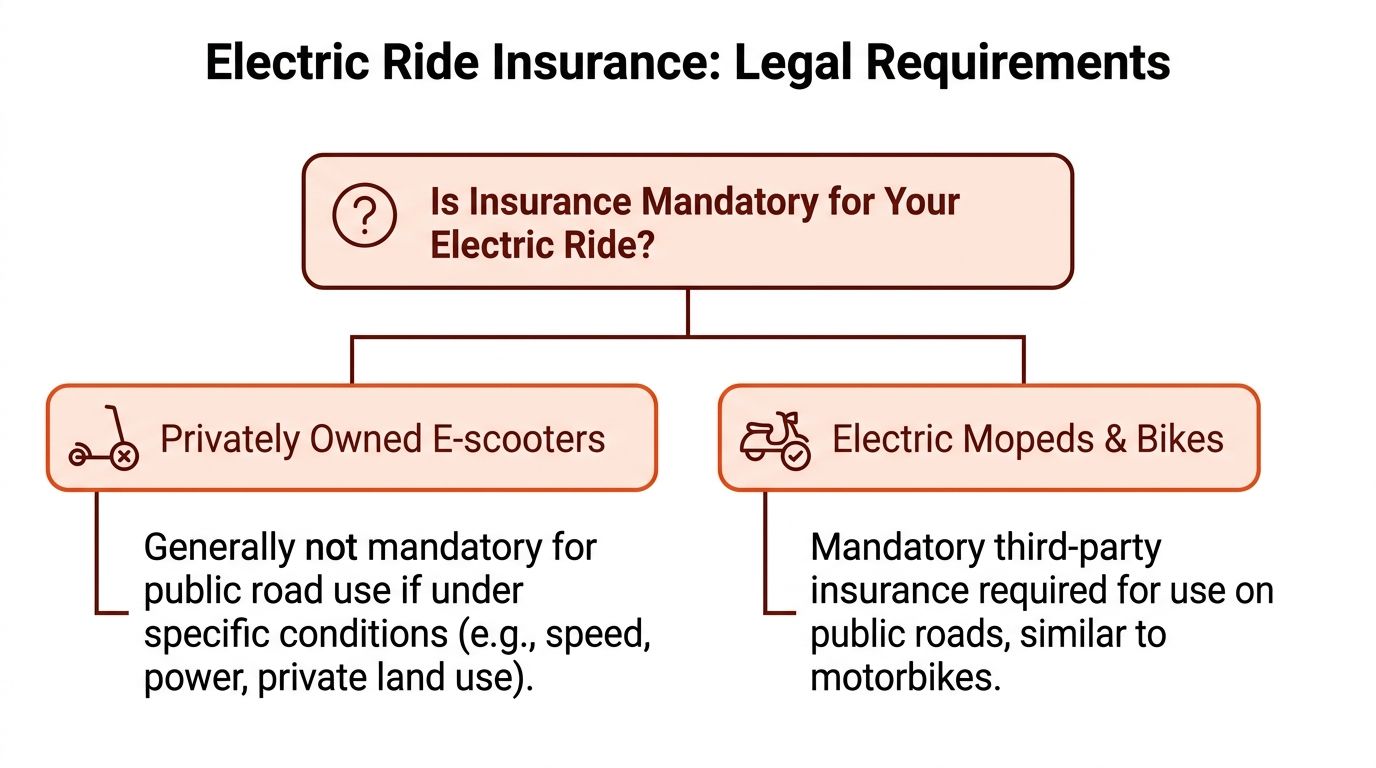

If you’re buying a road-legal electric moped or motorcycle in the UK, insurance is a legal requirement, and the minimum you need is third-party cover. That applies to road-legal electric mopeds and motorbikes in the same way it does to petrol machines, while privately owned stand-up e-scooters are still illegal to use on public roads and sit in a completely different category.

Most riders searching for insurance for electric scooters are really trying to answer a more practical question. “What do I need to ride legally, protect the bike, and avoid paying for the wrong policy?” That confusion is understandable because the internet is packed with generic advice about stand-up e-scooters, rental schemes, and overseas rules that don’t help when you’re insuring a UK-registered electric moped or motorcycle.

For UK riders, the key point is simple. If the machine is a road-legal electric moped or motorbike, insure it like a motor vehicle. If it’s a privately owned stand-up e-scooter, public-road use is a legal problem before insurance even enters the discussion.

This guide sticks to what matters for electric mopeds, electric motorcycles, off-road electric motorcycles, and kids motocross bikes. It cuts through the noise for commuters, delivery riders, and businesses that need the right cover rather than vague advice.

Table of Contents

- Personal cover for commuting and everyday riding

- Commercial cover for delivery work

- Fleet cover for business use

- Can I insure an off-road electric motorcycle on a normal road policy

- Do kids motocross bikes need insurance

- Will my battery be covered under insurance

- Can I start on personal cover and switch later if I begin delivery work

The Legal Landscape Is Insurance Mandatory for Your Electric Ride

The biggest mistake riders make is lumping every electric two-wheeler into one bucket. In UK law, that doesn’t work.

A road-legal electric moped or motorcycle is treated like a motor vehicle. A privately owned stand-up e-scooter is not treated the same way for public-road use, and that difference changes everything about insurance, registration, and legal riding.

What counts as a road-going electric vehicle

If your electric machine is built and approved for road use, it belongs in the same practical insurance conversation as a petrol scooter or motorbike. That means registration, the right licence or training, and proper motor insurance all matter.

Privately owned stand-up e-scooters create most of the confusion. The Department for Transport position remains that privately owned e-scooters are classed as Privately Owned Personal Light Electric Vehicles, and they remain illegal to ride on public roads, cycle paths, or pavements. That’s why generic articles about “scooter insurance” often send riders in the wrong direction.

If you’re registering and riding an electric moped or electric motorcycle on the road, think “motorbike insurance”, not gadget cover and not home insurance.

What the law requires

For electric scooters capable of exceeding 15.5 mph (25 km/h), UK rules treat them as Powered Transporters, which means at least third-party liability cover is required under the Road Traffic Act. Riding without it can lead to fines up to £300, vehicle seizure, and 6 penalty points on your licence, as outlined in this overview of UK e-scooter insurance rules.

For the kinds of road-legal electric mopeds and motorcycles UK riders register and insure, the practical takeaway is straightforward:

- Third-party cover is the legal floor: It protects other people if you cause injury or property damage.

- Road use triggers legal duties: If the bike is going on public roads, insurance isn’t optional.

- Private land is different: Off-road electric motorcycles and kids motocross bikes usually raise a different insurance question. That’s less about road traffic law and more about theft, damage, transport, and personal liability on private land or organised venues.

A lot of riders overcomplicate this part. You don’t need to become a legal expert. You need to identify the machine correctly.

Use this rule of thumb:

Vehicle typePublic road use in the UKInsurance positionRoad-legal electric mopedAllowed if properly registered and ridden legallyInsurance requiredRoad-legal electric motorcycleAllowed if properly registered and ridden legallyInsurance requiredPrivately owned stand-up e-scooterNot legal on public roads, cycle paths, or pavementsInsurance discussion is secondary to legalityOff-road electric motorcycleNot for public-road use unless separately road legalUsually specialist, storage, transport, or event-based coverKids motocross bikePrivate land or permitted venue useUsually not standard road insurance

That’s why insurance for electric scooters has to start with the vehicle category. Get that wrong, and everything else follows the wrong path.

Decoding Insurance Types Personal Commercial and Fleet Cover

Once you know the bike needs motor insurance, the next job is choosing the right policy class. Many claims problems arise when the policy class is incorrect. The bike is insured, but the use is declared wrongly.

For most buyers, the choice sits in one of three lanes. Personal, commercial, or fleet.

Personal cover for commuting and everyday riding

Personal or social-use cover suits riders using an electric moped or motorcycle for normal day-to-day travel. That usually means commuting, visiting friends, shopping, and general private riding.

This is often the cheapest starting point because the insurer sees a more predictable usage pattern. Shorter regular trips and non-commercial use usually produce fewer complications than all-day urban riding.

What personal cover does well:

- Covers ordinary riding use: commuting and social journeys

- Lets you choose the protection level: third-party only, third-party fire and theft, or full coverage

- Works for most non-business owners: especially first-time riders using 50cc or 125cc equivalent electric models

What it doesn’t do is cover income-generating riding. If you’re carrying food, parcels, or goods for work, personal cover on its own usually won’t match its actual use.

Commercial cover for delivery work

Food delivery riders need to be stricter with declarations than almost any other group. The machine may look identical to a commuter’s bike, but the insurer sees a different risk because the riding pattern is different.

Riders working on platforms such as Deliveroo and Uber Eats can face premiums up to 30% higher than standard personal policies because of frequent urban use and higher accident exposure. A 2025 DVLA report also noted a 45% rise in electric moped thefts in London, which makes theft protection and proper business-use cover harder to ignore, as discussed in this ABI premiums update.

Practical rule: If you earn money using the bike, tell the insurer exactly how. “Commuting” and “delivery work” are not interchangeable descriptions.

Commercial cover is the right fit when the bike is used for:

- Food delivery: meals, grocery drops, takeaway runs

- Courier work: local parcels or documents

- Business errands: work-related trips that go beyond ordinary commuting

The weak option is trying to save money by buying a personal policy and hoping it will do. That approach often looks cheaper on the quote screen and much worse when a claim lands.

Fleet cover for business use

Fleet insurance works best when a business runs more than one vehicle and wants one policy structure instead of separate rider-by-rider admin. Restaurants, florists, venues, and local delivery operators often end up here.

The advantage isn’t just convenience. Fleet cover gives a business a cleaner way to manage drivers, vehicles, business liability, and policy renewals under one system.

Here’s the side-by-side view.

FeaturePersonal / Social UseCommercial / Delivery UseBusiness FleetWho it’s forCommuters and private ridersDelivery riders and sole tradersBusinesses running multiple bikesTypical useSocial, domestic, commutingHire and reward, business use, delivery workMulti-rider operational useMain risk issueUnderinsuring theft or damageMisdeclared use and higher theft riskDriver management and policy controlBest fitOne rider, one bike, private useOne rider earning from the bikeSeveral bikes, business operationsWhat often goes wrongChoosing the cheapest cover onlyBuying personal cover for delivery useMixing personal and company use without clarity

Commercial and fleet buyers should also read the wording around goods carried, rider authorisation, overnight storage, and who is allowed to use each vehicle. Those details matter more than marketing labels.

What a Typical Electric Moped Policy Covers and Excludes

Insurance gets easier to compare when you stop reading it as legal jargon and start reading it as layers of protection. Most road-legal electric moped and motorcycle policies build in the same basic way.

Start with cover for other people. Add protection for your bike. Then check the small print that decides whether the insurer pays when something goes wrong.

The three main levels of cover

Third Party Only is the legal minimum. It covers injury or damage you cause to someone else, but it won’t usually pay to repair or replace your own bike.

Third Party, Fire and Theft adds protection if the bike is stolen or damaged by fire. For many urban riders, this is the middle ground that feels practical. It keeps you legal and adds some protection against the loss that hurts most.

Full coverage is the broadest standard option. It usually includes third-party liabilities plus cover for your own bike after an accident, subject to the policy wording, excess, conditions, and declared use.

A simple way to view it:

- Third Party Only: protects others

- TPFT: protects others, plus theft and fire

- Full Coverage: protects others and gives the widest protection for your own machine

Exclusions that catch riders out

Riders often assume they’re covered when they’re not.

Common exclusions and problem areas include:

- Wrong use declared: If the policy is set up for private riding and the bike is used for delivery work, that can cause serious trouble at claim stage.

- Security conditions ignored: Many insurers expect approved locks, secure parking, or evidence that the bike was stored as declared.

- Undeclared modifications: Screens, racks, performance changes, aftermarket alarms, and cosmetic extras can all matter.

- Battery disputes: Damage caused by an insured event may be covered, but normal deterioration or wear usually sits outside standard insurance thinking.

- Unlisted riders: If someone not named or not permitted under the certificate rides the bike, the policy may not respond as you expect.

The best policy on paper can still fail in real life if the usage, storage, or modifications weren’t disclosed properly.

This is also why it helps to think beyond the bike itself. Riders often understand the value of insuring a vehicle but ignore smaller, high-friction losses until they happen. If you want a useful example of how these niche add-ons are evaluated in the UK, this UK guide to car key cover is worth reading. The principle is the same. Cover is only useful when the wording matches the actual risk.

A practical buying habit works better than chasing the cheapest quote. Read the certificate, the schedule, and the exclusions. Then check whether they still make sense for how you ride.

Key Factors That Influence Your Insurance Premium

Insurers price three things first. The rider, the bike, and how the bike is used.

For a road-legal electric moped or motorcycle in the UK, that means two riders can insure the same model and still get very different quotes. A commuter riding a 50cc-equivalent electric moped to the station a few times a week presents a different risk from a delivery rider covering city miles every day. A business running several bikes has a different profile again.

Rider profile and where you live

Age, experience, claims history, and postcode all affect price. Theft rates, traffic density, and local claims patterns can push a premium up even before the insurer looks at the bike itself.

Newer riders usually pay more. So do riders with points, past claims, or a gap between their licence entitlement and the class of bike they want to insure. For electric mopeds and motorbikes, accuracy matters. If the insurer thinks you are quoting for one category but the registration or performance puts the bike in another, the price and the policy terms can change quickly.

The main rider factors are:

- Age and riding experience: Less experience usually means a higher premium

- Postcode: Urban theft risk and accident frequency often increase cost

- Claims and convictions: A cleaner record usually helps

- Licence category and training: The insurer needs the right entitlement for the exact bike

The bike itself matters

Electric two-wheelers are not grouped together in any useful insurance sense. That is where generic "electric scooter insurance" articles often go wrong. A road-legal electric moped sold for commuting is one risk. A faster electric motorcycle with a higher replacement value is another.

Insurers usually look at performance, top speed, replacement cost, parts availability, and theft appeal. ABS can help. So can factory-fitted security and a model with a sensible repair profile. Higher-value bikes and higher-performance bikes usually cost more to insure because claims tend to be larger when they are stolen or damaged.

A practical way to read this is simple:

Bike factorLikely insurance effectHigher performanceUsually pushes premiums upABS fittedMay help with insurer confidenceHigher replacement valueUsually increases the quotePopular theft targetCan increase the premiumFactory security featuresMay improve insurability and price

A practical video can help if you’re still comparing bike classes and insurance expectations:

Usage, storage and security

Usage has a big effect on premium because it changes exposure every day. Social riding, commuting, business use, and food delivery do not sit in the same risk bucket.

Delivery riders usually see higher prices because the bike is on the road more often, spends more time in busy urban areas, and is left unattended more frequently between stops. Commuters can still face high premiums if the bike is parked on the street overnight in a theft-heavy postcode. Fleet operators often get a different pricing approach again, because insurers assess driver controls, storage arrangements, and claims history across the whole business.

Storage and security are where riders can make practical gains. A locked garage usually helps more than street parking. Approved chains, anchors, alarms, or trackers can improve the quote, but only if they match what the insurer asks for and are in use.

A few trade-offs come up all the time:

- Higher excess for a lower premium: Works if you could afford that excess after a theft or crash

- Cheaper cover with weaker theft protection: Often poor value in city use

- Low declared mileage: Only useful if it reflects real usage

- Better overnight security: Often improves both price and insurer acceptance

The cheapest quote is rarely the best quote for an electric moped or motorbike that is used daily. Riders get better results by declaring the actual use case, choosing the right bike category, and setting up security that would still make sense on the day they need to claim.

Your Step-by-Step Guide to Getting Insured

Getting insured is usually straightforward when you prepare properly. It becomes messy when riders start comparing quotes before they’ve worked out the bike category, licence position, or intended use.

The cleanest route is to build your quote around accurate information from the start.

What to prepare before you compare quotes

Get the basics together first. For a road-legal electric moped or motorcycle, insurers usually want your personal details, address history, riding history, licence information, and the bike details.

Have these ready:

- Your licence and training details

Make sure your entitlement matches the vehicle you’re insuring. - The exact bike model

Use the correct make, model, and registration details if available. - Your intended use

Social use, commuting, business use, and delivery use are not the same thing. - Storage details

Be accurate about whether the bike is garaged, parked on a drive, or left on the street. - Security setup

Note any lock, chain, alarm, or tracker you’ll rely on.

If you’re insuring an off-road electric motorcycle or a kids motocross bike, the process changes. In those cases, ask specifically for cover that matches storage, transport, theft risk, event use, or private-land liability rather than assuming a standard road policy fits.

Buy the bike category first, then buy the matching insurance. Riders get into trouble when they force a road-use answer onto an off-road machine, or the other way round.

How to choose the right policy

Comparison websites are useful for a first pass, but they don’t always make specialist use cases clear. Delivery riding, business ownership, modified bikes, and unusual storage arrangements often benefit from a direct conversation with a broker or insurer.

When you review quotes, don’t just compare price. Compare what the policy expects from you.

Use this checklist before you buy:

Checklist for choosing your policy

- Check the declared use: private riding, commuting, business use, or delivery work

- Check the excess: make sure it’s realistic if you had to claim next week

- Check theft conditions: approved locks, alarm requirements, and storage wording

- Check named riders: especially for shared business use

- Check modifications: declare racks, boxes, screens, and accessories

- Check cover for accessories: helmets, luggage, or fitted extras may need to be specified

- Check legal assistance and breakdown options: useful, but only if they match how you ride

- Check renewal assumptions: don’t let an old mileage or usage estimate roll forward unchanged

A good buying decision often comes down to one question. If the bike were stolen or damaged tomorrow, would the insurer see the risk the same way you described it when you bought the policy? If the answer is yes, you’re usually on solid ground.

Managing a Claim and Proactively Reducing Your Risk

Claims are easier when the paperwork is right before anything goes wrong. That means the bike, rider, use, and storage all match the policy. After that, the best results usually come from staying calm, gathering evidence, and reporting the incident quickly.

The second half of the job is prevention. Riders who reduce theft exposure and avoid predictable accidents often protect both their no-claims history and their future premiums.

What to do after an accident or theft

After an accident, start with safety. Get clear of danger if possible, check for injuries, and contact emergency services if anyone needs help.

Then move into claim mode:

- Record the details: names, vehicle details, location, time, and any witness information

- Take photos: bike position, damage, road layout, and anything relevant nearby

- Notify the insurer promptly: don’t wait and don’t guess your way through the incident

- Stick to facts: avoid admitting liability at the roadside

- Keep documents together: photos, repair estimates, police reference if relevant, and correspondence

If the bike is stolen, report it to the police and your insurer as quickly as you can. Theft claims often turn on small details such as where the bike was parked, what security was in use, and whether the storage matched the policy declaration.

How different riders reduce risk

Different riders need different habits. One-size-fits-all advice usually isn’t much help.

For commuters, the biggest wins are consistency and visibility. Park in the same secure place where possible, use quality physical security every time, and avoid treating short stops as “safe enough” to skip the lock.

For delivery riders, discipline matters more than speed. The pressure to fit one more drop into a shift can push riders into bad parking choices, rushed U-turns, and tired decision-making. Business-use cover also needs regular review if your working pattern changes.

For business fleets, risk control is an operational issue, not just an insurance issue. Clear vehicle handover rules, authorised-rider records, regular maintenance checks, and route planning reduce friction when incidents happen. Telematics and rider training also help managers spot avoidable patterns such as harsh braking, poor parking habits, or inconsistent battery handling.

A claim is much easier to defend when the business can show who rode the bike, where it was stored, and how it was maintained.

For off-road electric motorcycles and kids motocross bikes, reducing risk usually means proper transport, secure storage, protective kit, and checking the venue or landowner’s rules before riding. Road-policy logic doesn’t always map neatly onto off-road use, so the rider who asks specific insurance questions early usually avoids expensive assumptions later.

Good insurance helps after an incident. Good habits reduce how often you need it.

Conclusion Your Ticket to Ride with Confidence

Insurance for electric scooters only makes sense in the UK when you separate road-legal electric mopeds and motorcycles from privately owned stand-up e-scooters. Once that distinction is clear, the rest becomes manageable.

If your electric moped or motorbike is going on public roads, insurance is part of legal ownership. After that, the main task is choosing the correct type of policy, accurately declaring the bike’s use, and reading the exclusions before they become a problem. Commuters, delivery riders, businesses, and off-road owners all need slightly different answers.

The best insurance isn’t the cheapest quote on the page. It’s the policy that still works when you need it.

If you want straight advice on choosing the right electric moped, motorcycle, or off-road model and understanding what ownership really involves, including insurance, maintenance, and setup, the team at Flex Electric can help.

Frequently Asked Questions About Electric Motorcycle Insurance

Can I insure an off-road electric motorcycle on a normal road policy

Usually not. Standard road insurance is set up for a road-legal, registered machine used on public roads with the correct class of use declared.

An off-road electric motorcycle raises different questions. Insurers will want to know where it is kept, how it is transported, who rides it, and whether you want cover for theft, accidental damage, or liability linked to private land or organised riding. If the bike is road-registered and fully approved for road use, you may be able to insure it on a normal motor policy. Check the bike’s status first rather than assuming the insurer will sort that distinction for you.

Do kids motocross bikes need insurance

Road insurance usually does not apply to kids electric motocross bikes because they are not being used as road-legal mopeds or motorcycles.

The practical question is what risk you want covered. For many parents, that means theft from a garage or van, crash damage, or protection while the bike is being transported to a track. Some also want liability cover linked to private land or organised riding. Asking for standard motorcycle insurance often sends you down the wrong path, because the cover needed is based on ownership and use, not road registration.

Will my battery be covered under insurance

It can be, but only if the policy includes it and the loss falls within an insured event.

A battery may be covered after theft, fire, or accident damage, depending on the wording and whether the battery is classed as part of the bike or as a separate item. Normal degradation, reduced range over time, poor charging practice, or warranty-type faults are usually not insurance matters. Keep those lines clear. Insurance handles sudden insured loss. The manufacturer warranty handles defects and performance issues covered by the warranty terms.

Can I start on personal cover and switch later if I begin delivery work

Yes, if you update the policy before you start using the bike for paid work.

This catches out riders who buy a road-legal electric moped for commuting, then pick up delivery shifts later. Delivery use changes the risk profile, and insurers rate it differently from social, domestic, pleasure, or standard commuting use. If you start food delivery or courier work without telling the insurer, a claim can become difficult very quickly. For riders using electric mopeds and motorcycles for work, getting the right class of use in place from day one is the safer approach.

Find us

You will find us at 74 Dalry Road, Edinburgh, EH11 2AY

Showroom Opening Times:

Monday: By Appointment

Tuesday to Friday: 11am - 5:00pm

Saturday: 10am - 5pm

Sunday: By Appointment