How to Get the Best Insurance Quote for Moped UK

Flex Electric

The UK's #1 Electric Moped and Electric Motorbike dealer.

Getting an insurance quote for a moped isn't just another task to tick off a list. It's about getting the right protection for your ride and, just as importantly, for your wallet. Let's walk through what you need to know to get it right.

Why Your Moped Insurance Quote Matters

First things first: you can't legally ride on UK roads without at least third-party insurance. It's the bare minimum. But getting insured goes far beyond just staying on the right side of the law.

Think about it. A good policy is your financial backstop if your electric moped or motorcycle is stolen, damaged, or you're involved in an accident. Without it, you’re personally on the hook for everything from repair bills to hefty liability claims, not to mention fines and points on your licence.

For those of us riding modern electrics—whether it's a nimble electric moped for city commuting or a powerful electric motorcycle for longer trips—that peace of mind is priceless. You’ve invested in a great machine; the right insurance makes sure that investment is properly protected.

And here’s some good news. While we often hear about insurance prices going up, the market for two-wheelers has seen some positive shifts. Increased competition means insurers are fighting for your business. In fact, figures show average motor insurance premiums actually dropped between early 2024 and late 2025. This is great for moped riders, as policies are already much cheaper than car insurance—you can often find basic cover for a 50cc-equivalent model for well under £300 a year. You can get a deeper dive into these figures in the latest UK motor insurance market report.

Choosing the right policy isn't just about meeting legal minimums. It's about creating a safety net that covers your specific riding habits, whether you're commuting, making deliveries, or enjoying a ride on an off-road electric motorcycle. A well-chosen policy protects you, your vehicle, and your financial future.

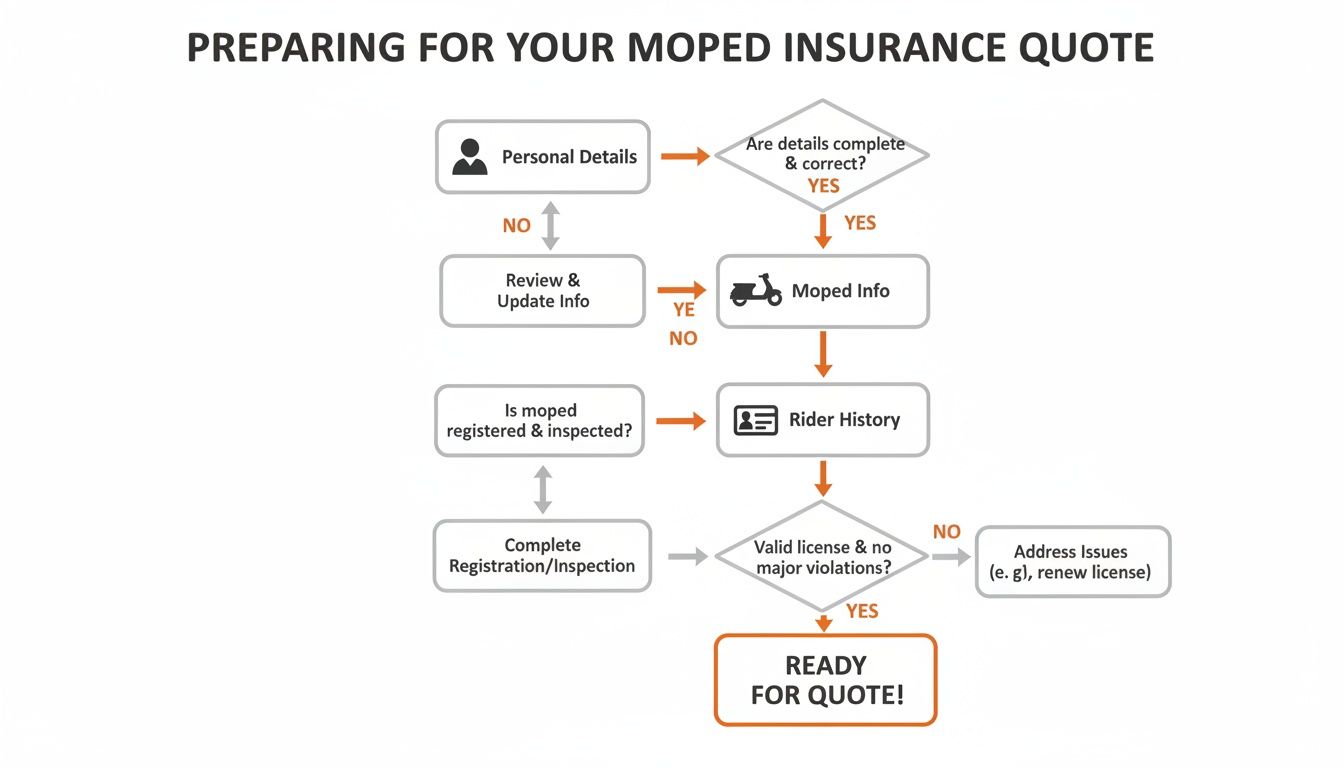

Preparing Your Details for an Accurate Quote

Getting a moped insurance quote shouldn't feel like pulling teeth. The secret to making it quick, painless, and—most importantly—accurate is to have all your information ready to go before you even start. Think of it as a pre-flight check. A few minutes of prep now will save you a ton of hassle and could even land you a much better price.

Insurers work on risk. The clearer the picture you can give them, the more confidence they'll have, which often translates into a more competitive quote. It shows you're on the ball.

Your Personal Information

Right, let's start with the basics about you. This information builds the foundation of your insurance profile.

- Full Name and Date of Birth: Your age plays a big part in the price you'll pay.

- Address and Postcode: Where you live and, crucially, where the vehicle will be kept overnight, directly impacts the premium. City centres are typically seen as higher risk than quiet, rural spots.

- Occupation: What you do for a living can also factor in, especially if your moped or motorcycle is part of your job.

Accuracy here is non-negotiable. A simple typo in your postcode or date of birth can throw the quote way off or, worse, invalidate your cover completely if you need to make a claim.

Your Rider History

Next, the insurer will want to get a feel for your experience on the road. This is all about them understanding what kind of rider you are.

A top tip is to have your driving licence number handy. It lets insurers look up your record in seconds, including any penalty points or convictions. You absolutely have to declare these – don't be tempted to hide anything.

This is also where your No-Claims Discount (NCD) comes into play. If you've been insured before and haven't made a claim, you can earn some serious discounts. After a few years, a solid NCD can slash your premium by over 50%. Make sure you have the proof from your last insurer ready to send over.

Finally, they’ll need to know about your licence. Whether you’re on a Compulsory Basic Training (CBT) certificate, an A1 licence, or have a full car licence from before 2001 (letting you ride certain 50cc-equivalents), it all affects your quote.

Details of Your Electric Moped or Motorcycle

The last piece of the puzzle is the vehicle itself. Insurers need to know exactly what they’re covering, right down to the last detail.

Get these specifics together:

- Make and Model: Be precise. A Super Soco CPx will be priced differently from a Horwin SK3. A high-performance machine like a LiveWire S2 is in a totally different league to a 50cc-equivalent city runabout. Even for kids' electric motocross bikes, the model matters.

- Registration Number: If you’ve already got the bike, this is the quickest way for an insurer to find its exact specs.

- Value and Age: Have a realistic figure for what your moped or motorcycle is worth on the market today.

- Security Measures: This is where you can save some money. List every approved lock, chain, immobiliser, or tracker you use.

- Storage: Tell them where it sleeps. Is it in a locked garage, on a private driveway, or parked on the street? Each one carries a different level of risk.

Choosing the Right Level of Insurance Cover

When you start looking for an insurance quote for a moped, it’s easy to get fixated on the price. But grabbing the absolute cheapest deal can be a false economy. That rock-bottom price usually gets you the bare minimum legal cover, which might not be enough to get you back on the road if something actually happens.

To make a smart choice, you need to understand what you're actually buying. Let’s break down the three main types of moped and electric motorcycle insurance in the UK, so you can find a policy that genuinely protects you and your ride, not just one that ticks a legal box.

Third-Party Only: The Legal Minimum

This is the most basic cover you can get, and it’s called Third-Party Only (TPO). In short, it’s designed to protect everyone else from you. If you cause an accident, it handles the costs for injuries to other people or damage to their property.

What it absolutely does not cover is your own moped or any injuries you suffer. If your electric motorcycle gets nicked or is damaged in a fire, you’re completely on your own. It's an option some riders with older, lower-value vehicles consider, where the cost of a higher-level policy might feel disproportionate to the vehicle's worth.

To get an accurate comparison of these different levels, you'll need to have some information handy first.

Getting your personal details, vehicle specs, and rider history sorted before you start makes the whole process of comparing quotes much smoother, regardless of which cover level you're leaning towards.

Third-Party, Fire and Theft: An Added Layer

The next level up is Third-Party, Fire and Theft (TPFT). This gives you everything the TPO policy does, but with the crucial addition of cover if your moped or motorcycle is stolen or damaged by fire.

It’s a popular middle-of-the-road choice, offering a bit more peace of mind, especially if you have to park your vehicle on the street overnight. Think of a casual rider with a new Horwin EK1 who uses it on weekends – TPFT strikes a good balance between cost and protection against common risks beyond an accident.

Fully Comprehensive: The Ultimate Protection

For the highest level of protection, you'll want Fully Comprehensive cover. This includes everything from a TPFT policy, but here’s the key difference: it also covers damage to your own vehicle in an accident, even if you were at fault.

Imagine a delivery rider on a Segway E110S navigating the chaos of Central London. That moped isn't just transport; it's their livelihood. For them, fully comprehensive cover is a business-critical investment, ensuring a minor prang doesn't mean they’re suddenly out of work.

I always recommend this for new or valuable electric mopeds, performance electric motorcycles, or for anyone who truly relies on their vehicle day in, day out. And here's a surprising tip: it isn't always the most expensive. Insurers sometimes view riders who opt for full cover as lower risk, which can lead to a more competitive insurance quote for your moped. It’s always worth checking the price difference.

Essential Policy Add-Ons

Once you've picked your core cover, you can often bolt on a few extras to fill in any gaps. These can be genuine lifesavers, depending on how you ride.

- Breakdown Assistance: If you commute or travel far from home, this is a must-have. Getting stranded with a dead battery or a puncture is no fun.

- Personal Accident Cover: This provides a financial payout if you’re seriously injured or worse in an accident, helping to cover costs when you can't work.

- Helmet and Leathers Cover: Good quality protective gear isn't cheap. This add-on helps you replace your helmet, jacket, and other kit if it gets ruined in an incident.

Take a moment to think about how you use your moped or motorcycle and weigh up whether the small extra cost for these add-ons is worth the peace of mind they provide.

What Factors Drive Your Moped Insurance Cost?

Ever looked at a moped insurance quote and wondered where on earth they got that number from? It’s not just plucked out of thin air. Insurers are essentially professional risk assessors, and your premium is the result of a detailed calculation that weighs up dozens of factors about you, your vehicle, and where you ride.

Getting a handle on these factors is your best bet for bringing that price down. Let's break down exactly what insurers are looking at when they draw up your quote.

Who You Are and Where You Ride

First things first, insurers look at you. Your personal details form the bedrock of their risk assessment. Unsurprisingly, age and riding experience are top of the list. A younger rider, especially one fresh off their CBT, is statistically more likely to be involved in an incident than a seasoned rider with years of no-claims bonus. It’s a simple numbers game for insurers, and it means higher premiums for newbies.

Your postcode is another massive piece of the puzzle. Living in a dense city centre, with its heavy traffic and higher crime statistics, will push your premium up compared to someone living in a sleepy village. Insurers use incredibly detailed geographical data to pinpoint the risk of theft and accidents right down to your specific street.

Finally, they need to know why you're riding. This is your 'class of use', and it makes a huge difference.

- Social, Domestic & Pleasure: This is the cheapest option, covering you for personal errands and leisure rides.

- Commuting: If you ride to and from a single, regular place of work, you’ll need to add this. The risk (and price) goes up slightly.

- Business Use: This is the big one. If you’re a delivery rider or use your moped for work appointments, you need specialist 'hire and reward' insurance. Expect a significant price jump, as your mileage and time spent in traffic are much higher.

Your Moped’s Specs and Security

Of course, the moped or motorcycle itself is just as crucial. A brand-new, high-performance electric motorcycle is going to cost a lot more to insure than a simple 50cc equivalent city runabout. The maths is straightforward: higher value, faster speeds, and more expensive repair costs all lead to a higher premium.

As a rule of thumb, the more powerful and valuable your moped or motorcycle, the more you'll pay to insure it. The insurer looks at its market value, top speed, and engine size (or electric equivalent) to calculate the risk.

But this is also where you can really start to fight back against high prices. Proving your vehicle is secure can shave a good chunk off your insurance quote for moped.

Insurers love to see that you’re taking theft prevention seriously. Make sure you tell them about every single security measure you have in place:

- Approved Security: Always mention any Thatcham-approved locks, ground anchors, chains, or alarms you use.

- Secure Storage: Parking in a locked garage overnight is the gold standard. A private driveway is good; on-street parking is the riskiest.

- Immobilisers & Trackers: If your vehicle has a factory-fitted immobiliser or you’ve added a tracker, it’s a major plus.

The rise of electric mopeds and motorcycles has also shaken things up. While they're brilliant for running costs, insurers are still getting to grips with new repair challenges, especially concerning batteries. This has put some upward pressure on premiums. A comprehensive policy for an electric moped from a brand like Segway or Horwin might fall in the £250-£400 annual range, but being smart with your security and cover level can keep you at the lower end of that scale. The wider UK motor insurance market is constantly shifting, as detailed in this market growth analysis.

To give you a clearer picture, we've broken down how these different elements can affect your final price.

How Different Factors Impact Your Premium

This table gives a quick overview of what insurers care about most and what you can do about it. A 'High' impact means this factor can dramatically swing your premium up or down.

.tbl-scroll{contain:inline-size;overflow-x:auto;-webkit-overflow-scrolling:touch}.tbl-scroll table{min-width:600px;width:100%;border-collapse:collapse;margin-bottom:20px}.tbl-scroll th{border:1px solid #ddd;padding:8px;text-align:left;background-color:#f2f2f2;white-space:nowrap}.tbl-scroll td{border:1px solid #ddd;padding:8px;text-align:left}FactorImpact LevelActionable Tip to Lower CostRider Age & ExperienceHighBuild a no-claims bonus over time. Taking an advanced riding course can sometimes help.Your PostcodeHighIf you have access to a more secure address (like a family home) to store the vehicle, use it.Claims HistoryHighRide safely and avoid making small claims to protect your no-claims bonus.Vehicle Value & PowerHighChoose a moped or motorcycle that fits your needs. A lower-powered, less expensive model is cheaper to insure.Overnight StorageMediumAlways store your vehicle in a locked garage if possible. It makes a real difference.Security DevicesMediumInvest in a Thatcham-approved lock, chain, or alarm. The discount often pays for the device.Class of UseHighBe honest about your usage. Don't pay for business use if you only ride for pleasure.Voluntary ExcessMediumAgreeing to a higher voluntary excess can lower your premium, but ensure you can afford it if you claim.

As you can see, some factors like your age are out of your control. However, focusing on the areas you can influence—like security, the type of vehicle you buy, and how much excess you're willing to pay—is the key to finding a quote that doesn't break the bank.

Ways to Bring Down Your Insurance Quote

Knowing what affects your premium is the first step. The real trick, though, is using that knowledge to your advantage. Getting a cheaper insurance quote for a moped isn't about ditching the cover you need; it’s about showing insurers you're a safe bet.

If you ride an electric moped or motorcycle—whether it's a zippy city model or a more powerful one—these are some of the best ways I’ve found to get a better price.

Guard Your No-Claims Bonus

Your no-claims bonus (NCB), sometimes called a no-claims discount, is easily your biggest money-saving asset. For every year you ride without making a claim, you'll get a discount. After about five years, this can knock up to 60% or more off your premium.

This is why you should always think twice before claiming for small scuffs or a cracked mirror. It often makes more financial sense to pay for minor repairs yourself. Doing so keeps your NCB intact, saving you a fortune in the long run.

Pro Tip: Consider paying a little extra to protect your no-claims bonus. This add-on usually lets you make one or two claims over a few years without resetting your discount back to zero. It's a small price for some serious peace of mind.

Bump Up Your Voluntary Excess

When you make a claim, the "excess" is the amount you contribute. This is split into two parts: a compulsory excess set by the insurer, and a voluntary excess you choose.

If you offer to pay a higher voluntary excess, you're telling the insurer you're prepared to take on a bit more of the risk yourself. They'll often thank you with a lower premium. The golden rule here is to only commit to an amount you could genuinely afford to pay out of pocket if something happened.

Pay for the Year Upfront

Spreading the cost of your insurance over monthly payments might seem easier on your wallet, but it's almost always more expensive. Insurers treat monthly payments like a loan, and they add interest for the convenience.

Paying for the full year in one go cuts out those financing charges. If you have the cash available, it’s one of the quickest and easiest wins for reducing your insurance quote for a moped.

Get an Advanced Riding Qualification

Insurers love riders who invest in their own skills. Taking an advanced rider course, like the ones offered by IAM RoadSmart or the BMF Blue Riband, is a brilliant way to prove you’re serious about safety.

Many providers recognise these qualifications and will offer a discount once you've passed. It’ll make you a better, more confident rider, and the insurance savings can often cover the cost of the course over a year or two.

Be Smart with Your Job Title

This one might surprise you, but how you describe your job matters. Be honest, of course, but think about the different ways you could accurately describe what you do. For example, a 'Chef' might pay more than a 'Kitchen Manager', simply because of how an insurer's data perceives the risk for each role.

There are online tools that let you compare insurance costs for different job titles. It's worth a quick search to see if a small, truthful tweak to your description could save you some money. Never lie about your profession, but exploring all the legitimate options is just smart shopping.

Your Moped Insurance Questions Answered

Even after you've gathered all your documents, a few common questions always seem to pop up right when you're ready to get a quote. Let's clear the air on some of the most frequent ones we hear from riders just like you.

What if I’m Using My Electric Moped for Food Delivery?

This is a big one. Your standard policy, often called Social, Domestic & Pleasure (even with commuting tacked on), simply won't cover you for delivering food. You'll need a specific commercial policy known as 'hire and reward' insurance.

Trying to get by on the wrong cover is a huge gamble. If you have a prang while on a delivery, your insurer will almost certainly invalidate your policy on the spot. That would leave you personally responsible for every penny of the costs, from vehicle damages to legal fees. Insurers know that delivery work means more miles in busy traffic, which equals higher risk. The premium is higher, but it's a non-negotiable for protecting yourself and staying on the right side of the law.

How Will Modifications Affect My Insurance Quote?

Anything you’ve changed from how the vehicle left the factory needs to be declared. We’re talking about everything from a performance chip or different gearing to purely cosmetic tweaks like a vinyl wrap or even just adding a top box.

The simple rule of thumb is: if it’s not standard, you must declare it. It's tempting to overlook small changes, but failing to mention a modification can give an insurer grounds to void your entire policy if you need to make a claim.

Unsurprisingly, performance upgrades will almost always push your premium up because they change the bike's risk profile. On the flip side, adding approved security gear, like a Thatcham-approved alarm or a tracker, can often earn you a nice little discount.

Can I Get a Quote Without a Registration Number?

Yes, you can, and it’s a smart move. Getting an insurance quote for a moped or motorcycle before you buy is the best way to budget properly. It lets you see the real-world cost difference between, say, a brand new Horwin EK1 and a Super Soco CU Mini.

Just give the insurer the exact make, model, and year of the vehicle you're considering. The price you get back will be an estimate, but in our experience, it's usually very accurate. You will, of course, need the official registration number before you can actually buy the policy and get on the road.

Is Insurance Cheaper for an Electric Moped Than a Petrol One?

When you’re looking at the popular 50cc and 125cc equivalent class, the answer is usually yes. Insurers are starting to see electric mopeds as a lower risk. They have fewer moving parts to go wrong, are stolen less often, and tend to be ridden by more safety-conscious individuals.

This often translates into a cheaper premium. That said, don't assume this applies to all electric bikes. A high-performance machine like a LiveWire S2 Del Mar has serious power and a high price tag, so its insurance premium will be right up there with powerful petrol equivalents.

Ready to make the switch? The team at Flex Electric lives and breathes electric bikes. We offer straight-talking advice to help you find the perfect ride for your commute, delivery round, or just for fun. Check out our hand-picked range of the UK's best electric mopeds and motorcycles. Find your next electric moped at Flex Electric.

Find us

You will find us at 74 Dalry Road, Edinburgh, EH11 2AY

Showroom Opening Times:

Monday: By Appointment

Tuesday to Friday: 11am - 5:00pm

Saturday: 10am - 5pm

Sunday: By Appointment