MX Bikes on Finance: Your 2026 UK Buying Guide

Flex Electric

The UK's #1 Electric Moped and Electric Motorbike dealer.

You're probably in one of three positions right now. You've found an electric off-road bike you want, your child has outgrown a smaller kids' MX model, or you need a practical electric moped or light motorcycle for work and the upfront price is the sticking point.

That's where finance earns its place. In the UK, electric bike buying has had a meaningful push from policy as well as product availability. The government's Plug-in Motorcycle Grant, introduced in 2016, historically offered 35% off the purchase price up to £500 for eligible zero-emission motorcycles and scooters, which made financed buying more practical by reducing the amount borrowed (UK Plug-in Motorcycle Grant background). Even though that support later changed, it helped establish electric two-wheelers as a serious finance category rather than a niche cash-only purchase.

This guide is only about electric motorcycles, mopeds, off-road electric motorcycles, and kids' motocross bikes. No electric bicycles, no vague lifestyle talk, and no pretending every rider fits the same finance model. A parent buying a youth bike, a weekend rider choosing a higher-spec electric MX machine, and a delivery rider protecting monthly cash flow all need different answers.

Table of Contents

Your Path to Owning an Electric MX Bike

You choose the bike for a reason. A parent wants something safe and manageable for weekend riding. A leisure rider wants better range, power, or build quality than the entry-level options. A delivery rider or small business needs a bike that can start earning quickly without draining working cash on day one. Then the full purchase price shows up, and the decision gets harder.

Finance helps when the bike is affordable over time but awkward as a one-off payment. For many buyers, that is the difference between buying the right machine now and settling for the wrong one, or waiting longer than they need to. The key is matching the agreement to how the bike will be used.

Earlier in the article, we mentioned the Plug-in Motorcycle Grant. Support like that has mattered because it cut the amount buyers needed to fund in the first place. Even without it, the same principle applies. The lower the amount financed, the less interest you pay and the easier the monthly commitment is to carry.

Practical rule: Finance works best when it fixes the upfront cash problem and still leaves you with a sensible total cost.

That last part gets missed. A low monthly payment can still be a poor deal if the term is too long, the deposit is too high for your cash flow, or the final cost no longer makes sense for the bike's job.

I see this most often with non-traditional buyers. A delivery rider may care less about cosmetic upgrades and more about keeping money available for insurance, charging, kit, and downtime. A small business may want a no-minimum-deposit option because tying up cash in the bike creates pressure elsewhere. For those buyers, flexible plans such as Flex Electric's no-minimum-deposit finance can solve a real business problem, but only if the monthly figure and the total repayable both stack up.

The rider's starting question

Most applications start with one clear question:

- Parent purchase: “Can I spread the cost of a kids' electric MX bike without making the agreement more complicated than it needs to be?”

- Leisure rider purchase: “Can I buy the spec I want now, and keep the payments at a level that feels comfortable?”

- Work-led purchase: “Can I keep cash in the business, avoid a large upfront payment, and still put a reliable electric bike into daily use?”

All three are sensible starting points. The right answer depends less on getting approved and more on choosing a finance product that fits your budget, your usage, and how long you expect to keep the bike.

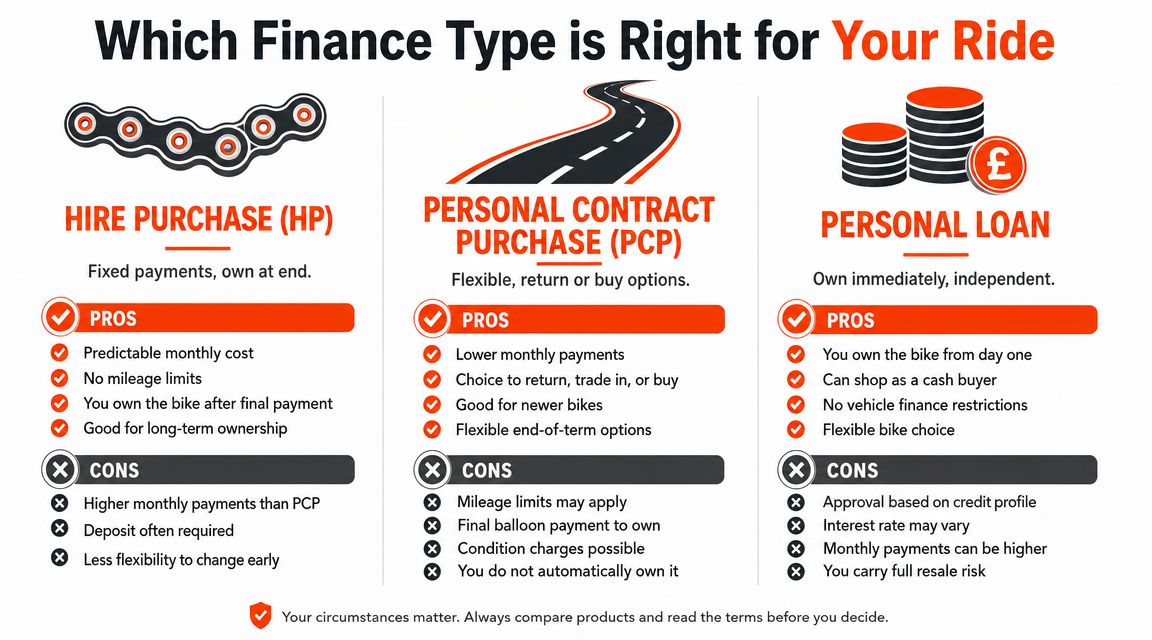

Understanding Your Electric Bike Finance Options

In the UK motorcycle market, the two finance products you'll see most often are Hire Purchase (HP) and Personal Contract Purchase (PCP). Both usually involve a deposit and fixed monthly payments, but the ending is different. With HP, you own the bike at the end. With PCP, you usually choose whether to pay a final balloon payment to keep it, trade it in, or hand it back (HP and PCP overview from a motorcycle finance page).

A personal loan sits outside dealer-style vehicle finance. It can still work well, but it behaves differently because the loan is between you and the lender rather than being secured in the same way against the bike.

How HP works in practice

HP is the cleanest option for most buyers who want ownership.

You pay a deposit, then fixed monthly instalments over an agreed term. Once the agreement is completed, the bike becomes yours. No final ownership choice to make, no mileage condition to worry about in the same way you would on a PCP.

Think of HP as a straight payment plan for a machine you fully intend to keep.

HP usually suits:

- Parents buying youth bikes: You want clarity, not flexibility games.

- Private riders keeping the bike long term: You're not planning to switch every few years.

- Buyers who dislike balloon payments: You'd rather see the full route to ownership from day one.

How PCP changes the cash flow

PCP changes the shape of the deal.

You still put down a deposit and make monthly payments, but you're not usually paying down the full value of the bike in the same way during the term. A larger amount can sit at the end as a balloon payment or Guaranteed Future Value style figure. That often lowers the monthly payment compared with HP on the same bike, but it also means the end-of-term choice matters more.

That's useful for riders who like flexibility. It's less useful for riders who assume the monthly figure tells the whole story.

Lower monthly payments can be sensible. They aren't automatically cheaper.

Here's the simplest comparison.

FeatureHire Purchase (HP)Personal Contract Purchase (PCP)DepositUsually requiredUsually requiredMonthly paymentsFixedFixedOwnership at endYes, after final paymentOnly if final balloon payment is madeEnd-of-term optionsKeep the bikeKeep, exchange, or hand backBest suited toBuyers focused on ownershipBuyers focused on flexibility and cash flow

Where a personal loan fits

A personal loan can be the right answer when dealer finance doesn't match the bike or the buyer.

That often comes up with pre-owned electric bikes, private sales, or buyers who want immediate ownership from the start. Because the purchase and the borrowing are separate, you can sometimes move faster on the bike itself. The trade-off is that your lender will assess you on its own criteria, and you won't get the same contract structure as HP or PCP.

A personal loan tends to work best when the bike is older, the seller isn't offering finance, or the buyer wants freedom over the asset from day one.

Which Finance Type is Right for Your Ride

There isn't one best answer for everyone. The right answer depends on what the bike needs to do for you, how long you expect to keep it, and how much flexibility matters compared with ownership.

Best fit by rider type

A parent buying a kids' electric MX bike usually wants simplicity. The child may move up to a different bike later, but the buying decision itself is rarely about complex end-of-term options. In those cases, HP often feels right because the route is obvious and the agreement is easy to understand.

A weekend rider choosing a more expensive electric off-road bike often has two competing goals. They want a stronger machine now, but they don't want to tie up all their spare cash in one purchase. That's where the choice between HP and PCP gets more personal. If you know you'll keep the bike, HP tends to be the cleaner fit. If you like changing bikes and want lower monthly strain, PCP can make sense.

Delivery riders and small businesses often care most about cash flow. Monthly affordability may matter more than eventual ownership, especially if the bike is there to support work rather than leisure. In that situation, PCP can be attractive, but only if the contract terms line up with real use.

What usually works and what usually doesn't

Here's the practical version.

- HP works well when you want predictable ownership and don't want an end-of-term decision hanging over you.

- PCP works well when lower monthly payments matter and you're comfortable with return, exchange, or balloon-payment choices later.

- Personal loans work well when the bike sits outside normal dealer finance routes, especially for some used purchases.

What usually causes regret is mismatch.

- Wrong for heavy-use riders: PCP can be awkward if your usage is hard to predict and contract restrictions don't fit.

- Wrong for short-term thinkers: HP can feel heavy if you know you'll want to change bikes quickly.

- Wrong for stretched budgets: Any finance product becomes a problem if the payment only works on a good month.

The best agreement is the one that still feels manageable when work slows down, riding plans change, or the bike needs attention.

Real World Costs How Much for an Electric MX Bike on Finance

The figures buyers focus on first are the same every time. Deposit. Monthly payment. Agreement length. APR. Those matter, but they don't matter equally.

A UK dealer example shows finance available on vehicles above £1,000, and a used-bike finance example shows a Representative APR of 9.4%. The same example references a bike priced at £6,846.99, which shows how finance can reduce upfront cash outlay while still making total cost of credit worth checking carefully (used motorcycle finance example and representative APR).

The figures that matter most

When I'm talking buyers through electric MX bikes on finance, I tell them to look at the deal in this order:

- Total amount repayable

This tells you what the borrowing costs. - Deposit flexibility

A no-minimum-deposit option can help access the bike sooner, but it usually changes the monthly and overall cost profile. - Term length

Stretching the term can improve monthly affordability, but it also keeps you in the agreement longer. - Bike suitability

Cheap monthly payments on the wrong machine are still a bad purchase.

If the bike is road-registered, buyers should also budget properly for the running side. For that part, a practical reference is this guide to UK vehicle tax rates 2026, especially if you're comparing a road-going electric motorcycle or moped with another type of vehicle expense.

Three realistic buying scenarios

The exact payment depends on lender criteria, deposit, term, and product type, so it's better to think in scenarios than assume one universal number.

Buyer scenarioTypical finance focusWhat to watchNew adult electric off-road bikeBalance of deposit and manageable monthly paymentWhether a lower monthly figure comes from a longer term or a balloon structurePre-owned electric modelAccess to stock that may sit outside standard new-bike promotionsCondition, age, and whether the finance route is HP, loan, or something more limitedNew kids' electric MX bikeSimplicity and short-to-medium term affordabilityAvoiding a finance structure that's more complex than the purchase needs

For buyers using no-minimum-deposit plans, the biggest benefit is obvious. You don't have to wait while you build a larger upfront lump sum. That can be the difference between buying now and postponing for months.

What doesn't work is judging affordability by the first monthly number you see on a website. The better test is this: if you add the deposit, monthly instalments, likely insurance, routine servicing, and expected wear items, does the bike still make sense for how often it will be used?

That question matters more on electric off-road and commuter machines than many people expect. If the bike will be used hard, used for work, or changed within a few years, the finance choice needs to support that reality.

How to Apply for Finance Eligibility and Documentation

Approval problems usually start long before the application is submitted. The issue isn't always bad credit. It's often poor preparation, inconsistent income evidence, or a buyer choosing the wrong product for their circumstances.

One of the biggest blind spots affects non-traditional applicants. Standard credit scoring doesn't always fit self-employed delivery riders with variable income, and affordability checks mean lenders want clear proof of what you earn, not what you estimate you earn (finance eligibility challenge for variable-income riders).

What lenders usually want to see

Most applications become easier when the basics are organised before you start.

- Proof of identity: Driving licence or other accepted photo ID.

- Proof of address: Utility bill, bank statement, or similar recent document.

- Income evidence: Payslips if employed, or a clear record of earnings if self-employed.

- Banking consistency: An account history that supports the affordability picture shown in the application.

For employed applicants, that can be fairly straightforward. For self-employed riders, the burden is different. Lenders often want to see that your income is regular enough to support the agreement, even if the amounts vary from week to week.

Bring clean paperwork, not explanations. Lenders can work with variable income more easily than they can work with missing evidence.

Extra preparation for delivery riders and small businesses

If you're a delivery rider working across apps, don't rely on screenshots alone unless the lender or broker says they'll accept them. A stronger file usually includes bank statements showing incoming payments, tax documentation where available, and account records that match the income declared.

Small businesses financing electric mopeds or light motorcycles for staff need a different approach. The application may depend on trading history, business banking, and whether the finance sits in the company name or with a director support element. The cleaner the paperwork, the smoother the process.

A sensible prep checklist looks like this:

- For delivery riders: Gather bank statements, platform earnings summaries, and any recent tax documents.

- For sole traders: Make sure declared income and banked income line up.

- For limited companies: Prepare company details, trading evidence, and proof of who is authorised to sign.

- For all applicants: Check your address history is accurate and consistent across forms.

This short video gives a useful overview of how people commonly approach finance paperwork and review stages before signing:

If you think you may be borderline for approval, the worst move is applying blindly to several providers at once. A better move is to get your documents in order, be realistic about the bike and price point, and choose a finance route that matches how you earn.

Key Details to Check Before You Sign

A parent buying a first electric MX bike, a weekend rider upgrading to something faster, and a delivery rider putting a bike to work can all be shown the same monthly payment. That does not mean the deal fits all three buyers equally well.

The agreement matters more than the headline figure. I tell customers to read the finance document as if they are buying two things at once: the bike itself and the terms wrapped around it. Monthly cost is only one part of the decision. Total amount repayable, deposit, term length, final payment if there is one, usage limits, and what happens if your plans change all affect whether the deal still feels right six months in.

The monthly payment trap

A low monthly payment usually comes from one of four places:

- A longer agreement term

- A larger final payment on PCP

- A bigger deposit

- More cost pushed to the back end of the agreement

Each option can be sensible. The problem is signing without knowing which one is doing the work.

That matters even more for non-traditional buyers. A delivery rider might prefer a no-minimum-deposit option to protect cash flow, but that can mean higher monthly payments or more interest across the term. A small business may want lower month-to-month cost for fleet budgeting, but a mileage cap or hand-back condition clause can create problems if the bikes are used hard. The right answer depends on how the bike earns its keep, not just whether the first payment looks comfortable.

If you're reviewing documents digitally, it helps to know how the process works before you commit. This e-signing documents guide is useful for understanding how to review and sign finance paperwork carefully rather than clicking through too quickly.

Contract points worth slowing down for

Read these parts properly before you sign:

- Total amount repayable: This is the figure that shows what the bike costs over the full agreement.

- Early settlement terms: Check what happens if you want to clear the balance sooner.

- Mileage conditions on PCP: Important for commuters, couriers, and anyone using the bike regularly for work.

- Condition standards at hand-back: Scratches, wear, tyres, and general use can matter if you are not keeping the bike.

- Final payment amount: Make sure the optional balloon payment is realistic if ownership is the plan.

- Warranty and after-sales support: A good agreement looks very different if the bike needs attention during the finance term.

One weak point can wipe out the benefit of a cheap monthly figure.

I see this most often with working riders and business buyers. They focus on getting approved quickly, then only later realise the agreement assumed lighter use, cleaner end-of-term condition, or a larger final payment than they had budgeted for. Flexible structures such as no-minimum-deposit plans can be very useful, especially when cash needs to stay in the business or available for kit, insurance, and running costs. They still need checking line by line.

A good finance deal should suit the way the bike will be used, and still look fair once you add up the full cost.

Get on the Track with Smart Finance

Buying an electric MX bike, moped, or off-road motorcycle on finance isn't about chasing the lowest monthly figure. It's about matching the finance product to the way you'll use the bike.

If ownership is the priority, HP usually gives the clearest path. If flexibility and lower monthly pressure matter more, PCP can work well when the end-of-term terms suit your riding. If you're buying pre-owned or outside a standard dealer setup, a personal loan can still be the right tool.

The buyers who make the best decisions usually do three things well. They choose the bike for the job, they check the total repayable instead of fixating on the monthly payment, and they prepare their documents properly before applying.

That approach works whether you're buying a child's first electric MX bike, upgrading your own off-road machine, or adding an electric work bike to a delivery setup. Good finance should make the bike more accessible, not more confusing.

If you want straight answers on electric motorcycles, mopeds, off-road bikes, and kids' MX models, Flex Electric is a strong place to start. They offer practical guidance, UK-wide delivery, flexible HP and PCP options with no minimum deposit required, and after-sales support that matters once the agreement is live.

Find us

You will find us at 74 Dalry Road, Edinburgh, EH11 2AY

Showroom Opening Times:

Monday: By Appointment

Tuesday to Friday: 11am - 5:00pm

Saturday: 10am - 5pm

Sunday: By Appointment